Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeEnhancing reliability in prediction intervals using point forecasters: Heteroscedastic Quantile Regression and Width-Adaptive Conformal Inference

Jun 21, 2024Building prediction intervals for time series forecasting problems presents a complex challenge, particularly when relying solely on point predictors, a common scenario for practitioners in the industry. While research has primarily focused on achieving increasingly efficient valid intervals, we argue that, when evaluating a set of intervals, traditional measures alone are insufficient. There are additional crucial characteristics: the intervals must vary in length, with this variation directly linked to the difficulty of the prediction, and the coverage of the interval must remain independent of the difficulty of the prediction for practical utility. We propose the Heteroscedastic Quantile Regression (HQR) model and the Width-Adaptive Conformal Inference (WACI) method, providing theoretical coverage guarantees, to overcome those issues, respectively. The methodologies are evaluated in the context of Electricity Price Forecasting and Wind Power Forecasting, representing complex scenarios in time series forecasting. The results demonstrate that HQR and WACI not only improve or achieve typical measures of validity and efficiency but also successfully fulfil the commonly ignored mentioned characteristics.

An adaptive standardisation model for Day-Ahead electricity price forecasting

Nov 05, 2023

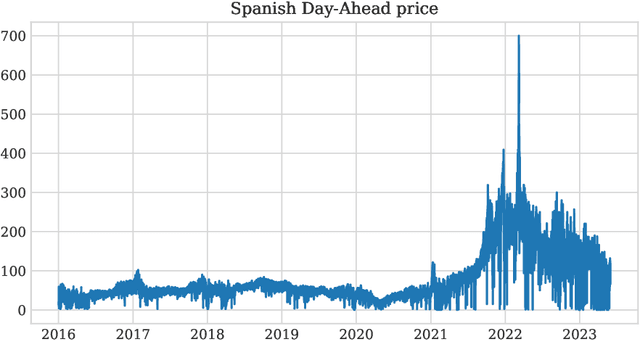

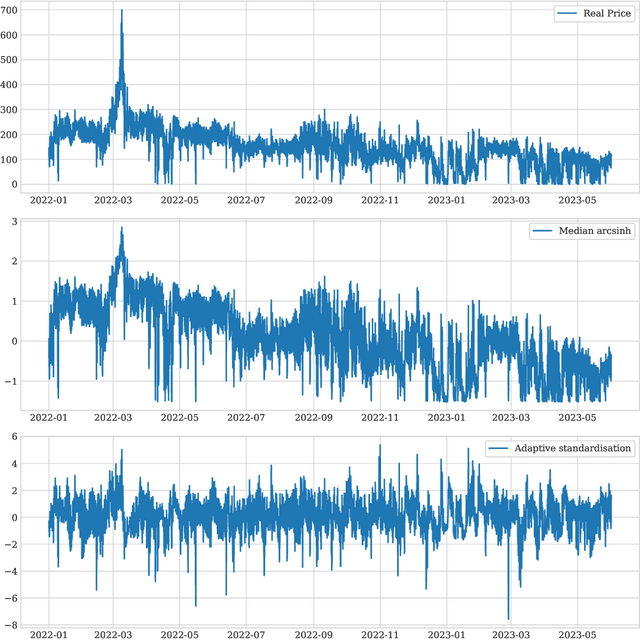

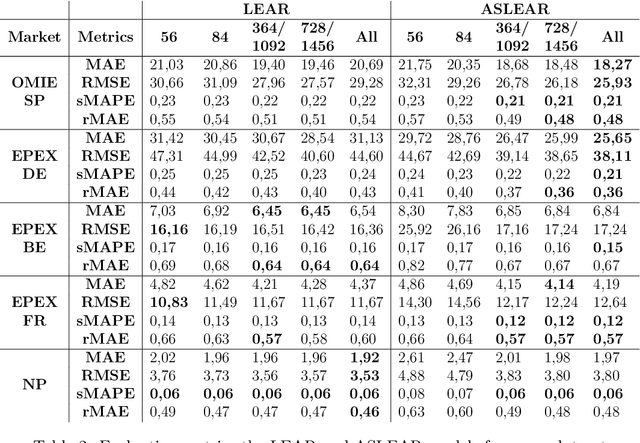

The study of Day-Ahead prices in the electricity market is one of the most popular problems in time series forecasting. Previous research has focused on employing increasingly complex learning algorithms to capture the sophisticated dynamics of the market. However, there is a threshold where increased complexity fails to yield substantial improvements. In this work, we propose an alternative approach by introducing an adaptive standardisation to mitigate the effects of dataset shifts that commonly occur in the market. By doing so, learning algorithms can prioritize uncovering the true relationship between the target variable and the explanatory variables. We investigate four distinct markets, including two novel datasets, previously unexplored in the literature. These datasets provide a more realistic representation of the current market context, that conventional datasets do not show. The results demonstrate a significant improvement across all four markets, using learning algorithms that are less complex yet widely accepted in the literature. This significant advancement unveils opens up new lines of research in this field, highlighting the potential of adaptive transformations in enhancing the performance of forecasting models.