Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeA Data-driven Market Simulator for Small Data Environments

Jun 21, 2020

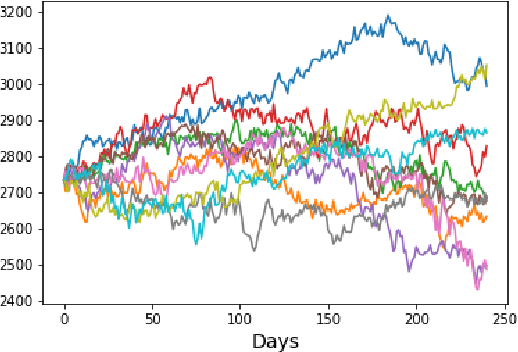

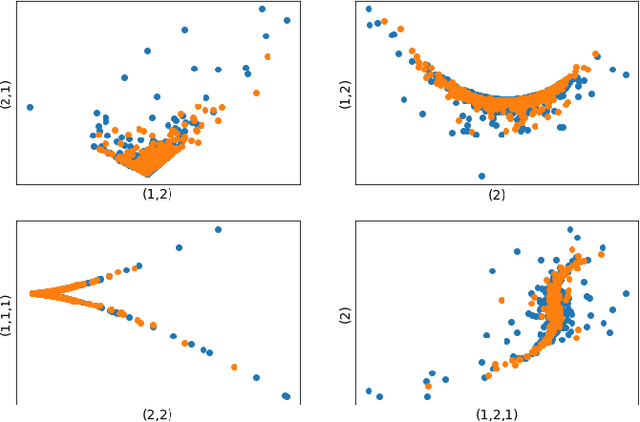

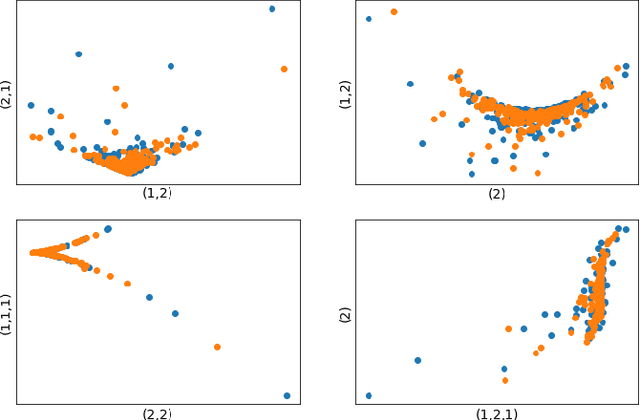

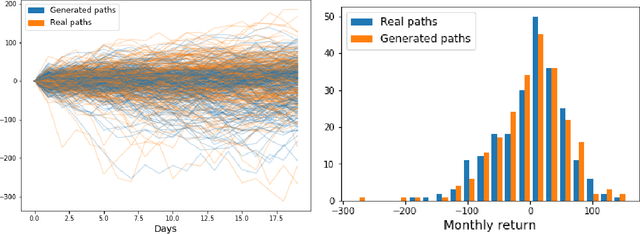

Neural network based data-driven market simulation unveils a new and flexible way of modelling financial time series without imposing assumptions on the underlying stochastic dynamics. Though in this sense generative market simulation is model-free, the concrete modelling choices are nevertheless decisive for the features of the simulated paths. We give a brief overview of currently used generative modelling approaches and performance evaluation metrics for financial time series, and address some of the challenges to achieve good results in the latter. We also contrast some classical approaches of market simulation with simulation based on generative modelling and highlight some advantages and pitfalls of the new approach. While most generative models tend to rely on large amounts of training data, we present here a generative model that works reliably in environments where the amount of available training data is notoriously small. Furthermore, we show how a rough paths perspective combined with a parsimonious Variational Autoencoder framework provides a powerful way for encoding and evaluating financial time series in such environments where available training data is scarce. Finally, we also propose a suitable performance evaluation metric for financial time series and discuss some connections of our Market Generator to deep hedging.