Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeHigh-performance stock index trading: making effective use of a deep LSTM neural network

Feb 07, 2019

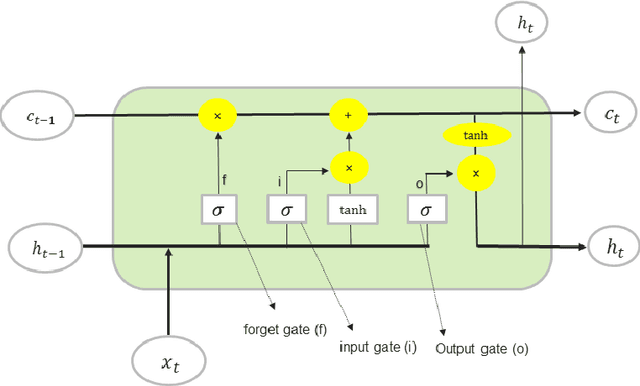

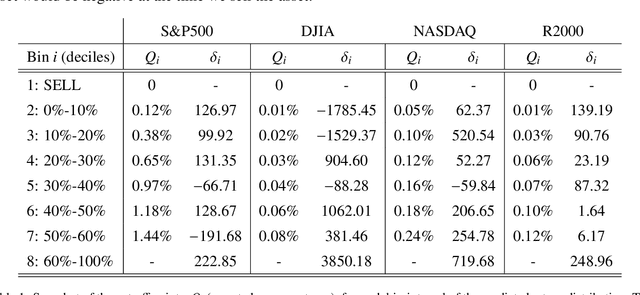

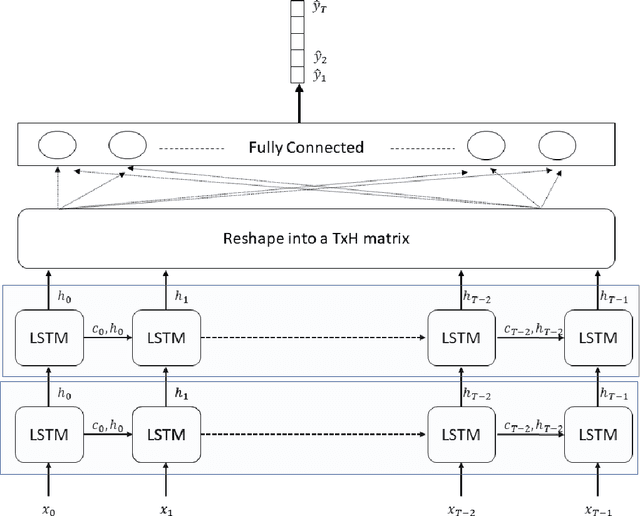

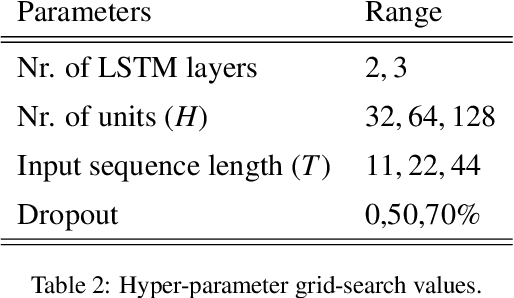

We present a deep long short-term memory (LSTM)-based neural network for predicting asset prices, together with a successful trading strategy for generating profits based on the model's predictions. Our work is motivated by the fact that the effectiveness of any prediction model is inherently coupled to the trading strategy it is used with, and vise versa. This highlights the difficulty in developing models and strategies which are jointly optimal, but also points to avenues of investigation which are broader than prevailing approaches. Our LSTM model is structurally simple and generates predictions based on price observations over a modest number of past trading days. The model's architecture is tuned to promote profitability, as opposed to accuracy, under a strategy that does not trade simply based on whether the price is predicted to rise or fall, but rather takes advantage of the distribution of predicted returns, and the fact that a prediction's position within that distribution carries useful information about the expected profitability of a trade. The proposed model and trading strategy were tested on the S&P 500, Dow Jones Industrial Average (DJIA), NASDAQ and Russel 2000 stock indices, and achieved cumulative returns of 329%, 241%, 468% and 279%, respectively, over 2010-2018, far outperforming the benchmark buy-and-hold strategy as well as other recent efforts.

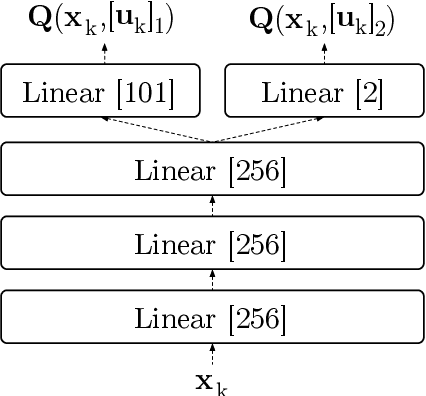

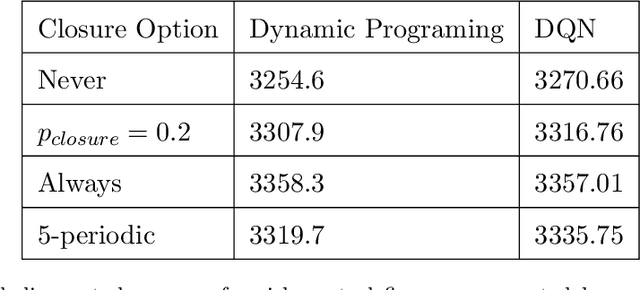

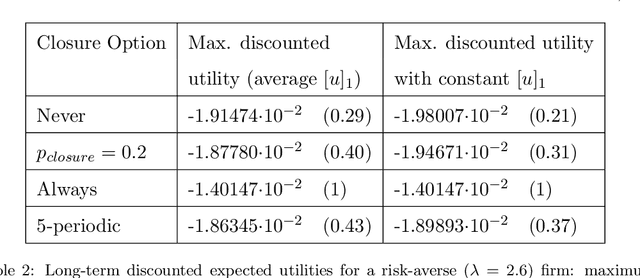

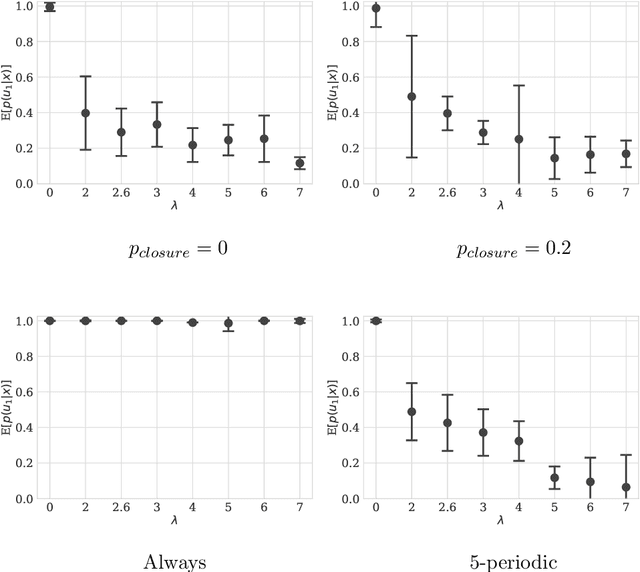

Using deep Q-learning to understand the tax evasion behavior of risk-averse firms

Jan 29, 2018

Designing tax policies that are effective in curbing tax evasion and maximize state revenues requires a rigorous understanding of taxpayer behavior. This work explores the problem of determining the strategy a self-interested, risk-averse tax entity is expected to follow, as it "navigates" - in the context of a Markov Decision Process - a government-controlled tax environment that includes random audits, penalties and occasional tax amnesties. Although simplified versions of this problem have been previously explored, the mere assumption of risk-aversion (as opposed to risk-neutrality) raises the complexity of finding the optimal policy well beyond the reach of analytical techniques. Here, we obtain approximate solutions via a combination of Q-learning and recent advances in Deep Reinforcement Learning. By doing so, we i) determine the tax evasion behavior expected of the taxpayer entity, ii) calculate the degree of risk aversion of the "average" entity given empirical estimates of tax evasion, and iii) evaluate sample tax policies, in terms of expected revenues. Our model can be useful as a testbed for "in-vitro" testing of tax policies, while our results lead to various policy recommendations.