Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeHigh-performance stock index trading: making effective use of a deep LSTM neural network

Feb 07, 2019

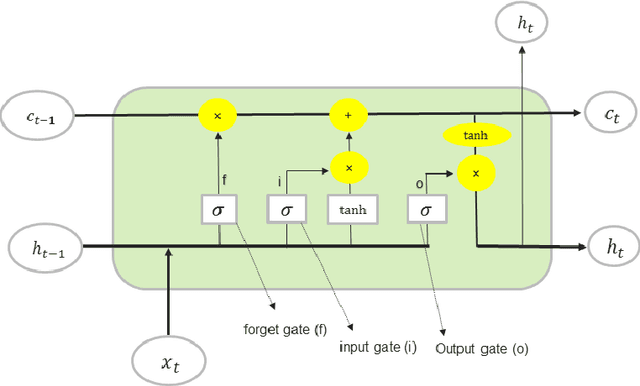

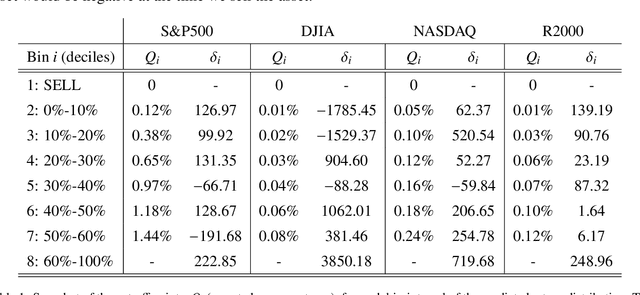

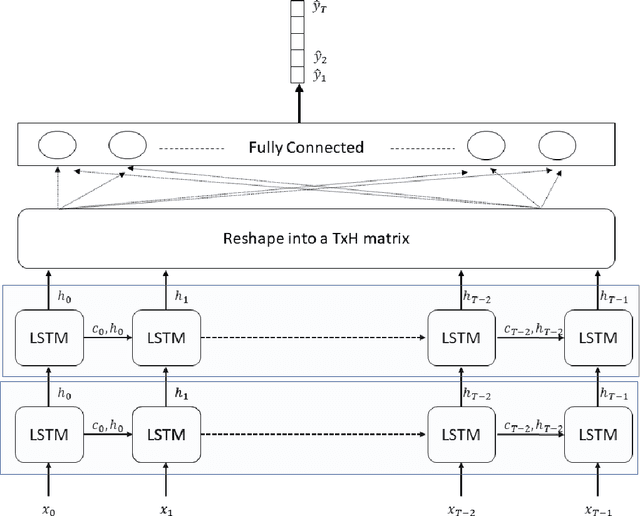

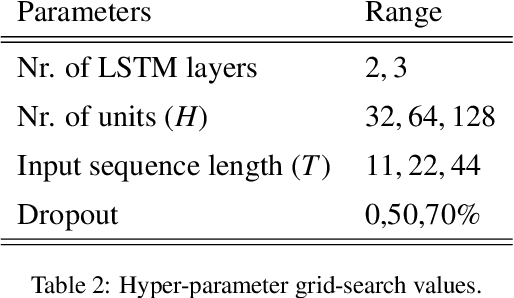

We present a deep long short-term memory (LSTM)-based neural network for predicting asset prices, together with a successful trading strategy for generating profits based on the model's predictions. Our work is motivated by the fact that the effectiveness of any prediction model is inherently coupled to the trading strategy it is used with, and vise versa. This highlights the difficulty in developing models and strategies which are jointly optimal, but also points to avenues of investigation which are broader than prevailing approaches. Our LSTM model is structurally simple and generates predictions based on price observations over a modest number of past trading days. The model's architecture is tuned to promote profitability, as opposed to accuracy, under a strategy that does not trade simply based on whether the price is predicted to rise or fall, but rather takes advantage of the distribution of predicted returns, and the fact that a prediction's position within that distribution carries useful information about the expected profitability of a trade. The proposed model and trading strategy were tested on the S&P 500, Dow Jones Industrial Average (DJIA), NASDAQ and Russel 2000 stock indices, and achieved cumulative returns of 329%, 241%, 468% and 279%, respectively, over 2010-2018, far outperforming the benchmark buy-and-hold strategy as well as other recent efforts.