Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeCan ChatGPT Compute Trustworthy Sentiment Scores from Bloomberg Market Wraps?

Jan 09, 2024

We used a dataset of daily Bloomberg Financial Market Summaries from 2010 to 2023, reposted on large financial media, to determine how global news headlines may affect stock market movements using ChatGPT and a two-stage prompt approach. We document a statistically significant positive correlation between the sentiment score and future equity market returns over short to medium term, which reverts to a negative correlation over longer horizons. Validation of this correlation pattern across multiple equity markets indicates its robustness across equity regions and resilience to non-linearity, evidenced by comparison of Pearson and Spearman correlations. Finally, we provide an estimate of the optimal horizon that strikes a balance between reactivity to new information and correlation.

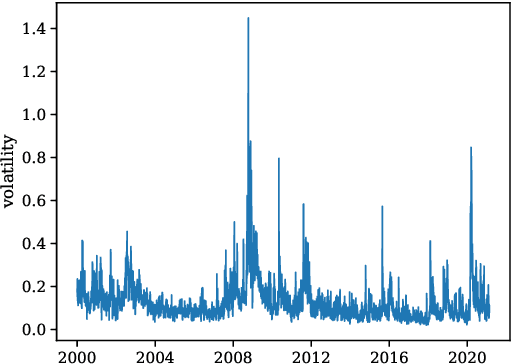

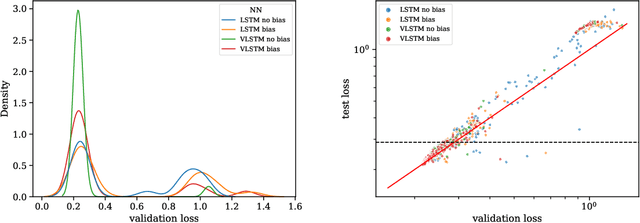

Recurrent Neural Networks with more flexible memory: better predictions than rough volatility

Aug 04, 2023

We extend recurrent neural networks to include several flexible timescales for each dimension of their output, which mechanically improves their abilities to account for processes with long memory or with highly disparate time scales. We compare the ability of vanilla and extended long short term memory networks (LSTMs) to predict asset price volatility, known to have a long memory. Generally, the number of epochs needed to train extended LSTMs is divided by two, while the variation of validation and test losses among models with the same hyperparameters is much smaller. We also show that the model with the smallest validation loss systemically outperforms rough volatility predictions by about 20% when trained and tested on a dataset with multiple time series.

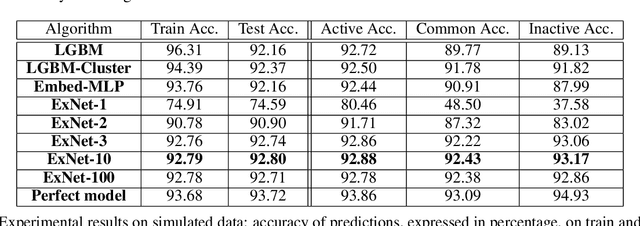

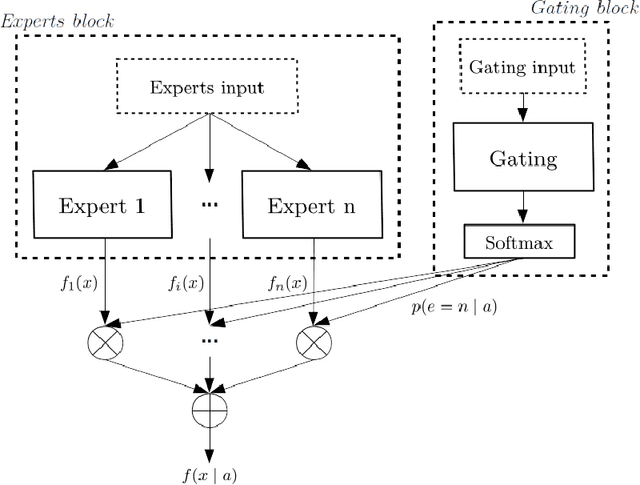

Deep Prediction of Investor Interest: a Supervised Clustering Approach

Sep 11, 2019

We propose a novel deep learning architecture suitable for the prediction of investor interest for a given asset in a given timeframe. This architecture performs both investor clustering and modelling at the same time. We first verify its superior performance on a simulated scenario inspired by real data and then apply it to a large proprietary database from BNP Paribas Corporate and Institutional Banking.