Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeImpact of the COVID-19 outbreak on Italy's country reputation and stock market performance: a sentiment analysis approach

Mar 13, 2021

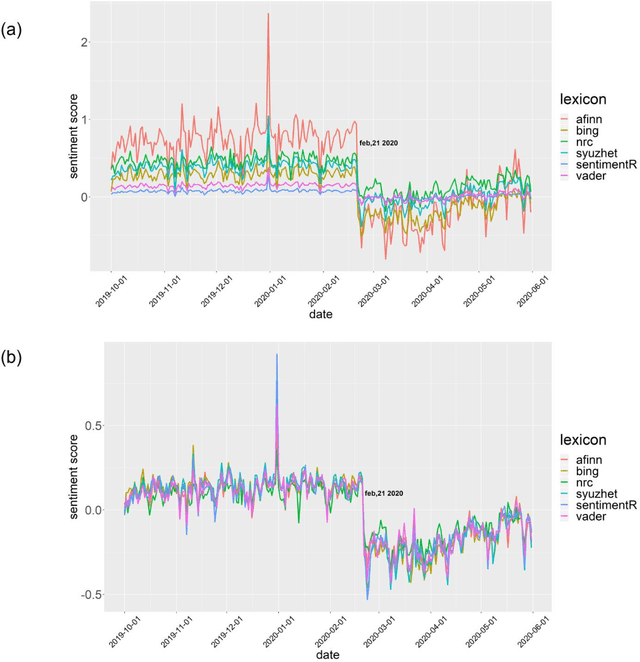

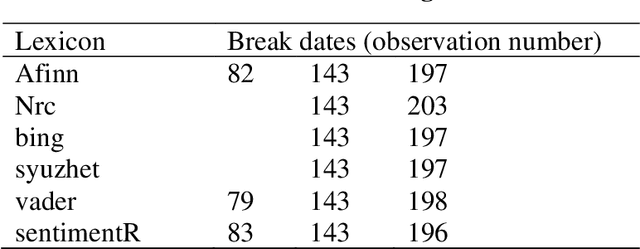

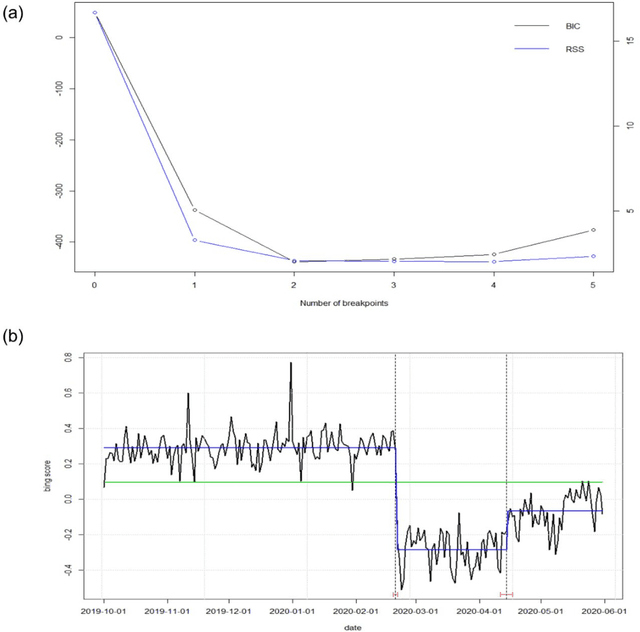

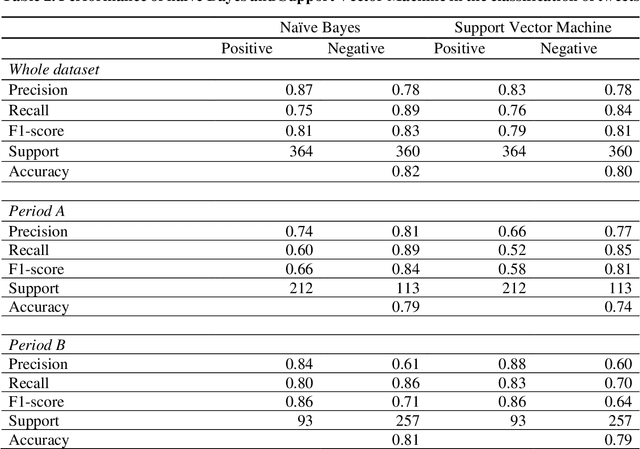

During the recent Coronavirus disease 2019 (COVID-19) outbreak, the microblogging service Twitter has been widely used to share opinions and reactions to events. Italy was one of the first European countries to be severely affected by the outbreak and to establish lockdown and stay-at-home orders, potentially leading to country reputation damage. We resort to sentiment analysis to investigate changes in opinions about Italy reported on Twitter before and after the COVID-19 outbreak. Using different lexicons-based methods, we find a breakpoint corresponding to the date of the first established case of COVID-19 in Italy that causes a relevant change in sentiment scores used as proxy of the country reputation. Next, we demonstrate that sentiment scores about Italy are strongly associated with the levels of the FTSE-MIB index, the Italian Stock Exchange main index, as they serve as early detection signals of changes in the values of FTSE-MIB. Finally, we make a content-based classification of tweets into positive and negative and use two machine learning classifiers to validate the assigned polarity of tweets posted before and after the outbreak.

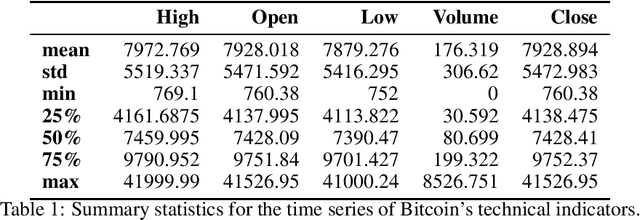

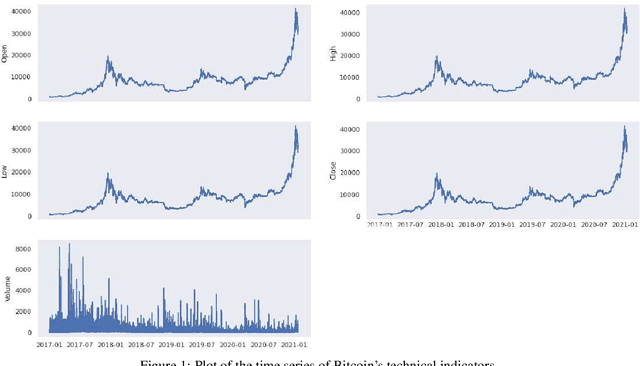

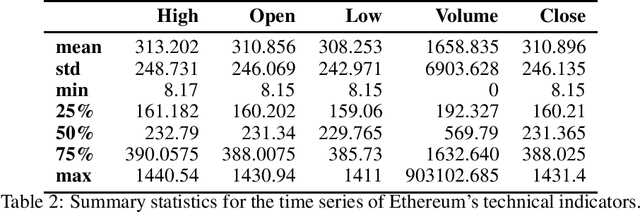

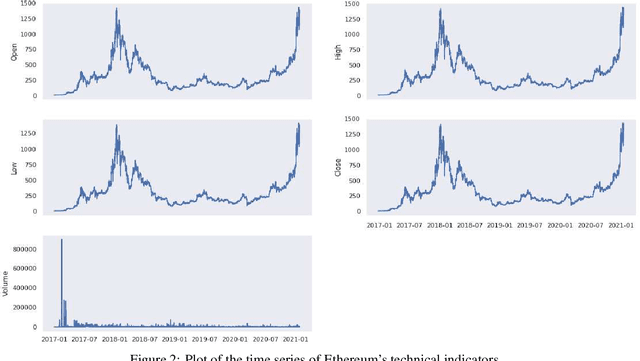

On Technical Trading and Social Media Indicators in Cryptocurrencies' Price Classification Through Deep Learning

Feb 17, 2021

This work aims to analyse the predictability of price movements of cryptocurrencies on both hourly and daily data observed from January 2017 to January 2021, using deep learning algorithms. For our experiments, we used three sets of features: technical, trading and social media indicators, considering a restricted model of only technical indicators and an unrestricted model with technical, trading and social media indicators. We verified whether the consideration of trading and social media indicators, along with the classic technical variables (such as price's returns), leads to a significative improvement in the prediction of cryptocurrencies price's changes. We conducted the study on the two highest cryptocurrencies in volume and value (at the time of the study): Bitcoin and Ethereum. We implemented four different machine learning algorithms typically used in time-series classification problems: Multi Layers Perceptron (MLP), Convolutional Neural Network (CNN), Long Short Term Memory (LSTM) neural network and Attention Long Short Term Memory (ALSTM). We devised the experiments using the advanced bootstrap technique to consider the variance problem on test samples, which allowed us to evaluate a more reliable estimate of the model's performance. Furthermore, the Grid Search technique was used to find the best hyperparameters values for each implemented algorithm. The study shows that, based on the hourly frequency results, the unrestricted model outperforms the restricted one. The addition of the trading indicators to the classic technical indicators improves the accuracy of Bitcoin and Ethereum price's changes prediction, with an increase of accuracy from a range of 51-55% for the restricted model, to 67-84% for the unrestricted model.