Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeSome machine learning schemes for high-dimensional nonlinear PDEs

Feb 05, 2019

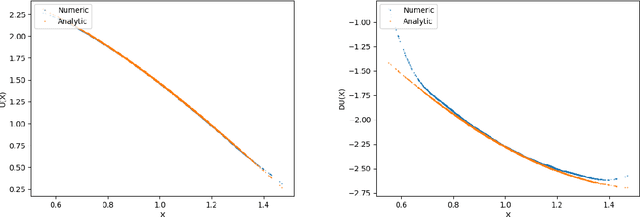

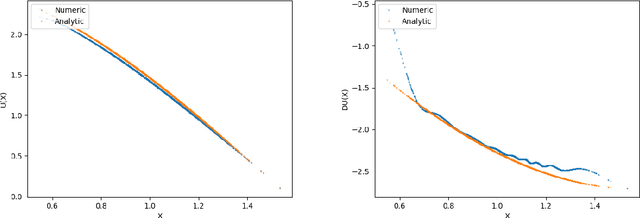

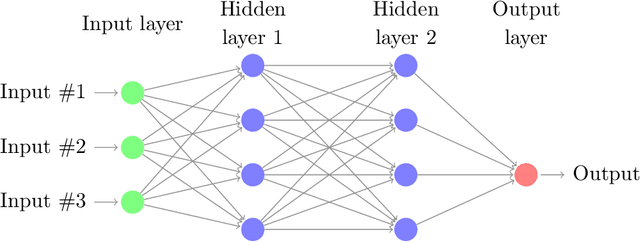

We propose new machine learning schemes for solving high dimensional nonlinear partial differential equations (PDEs). Relying on the classical backward stochastic differential equation (BSDE) representation of PDEs, our algorithms estimate simultaneously the solution and its gradient by deep neural networks. These approximations are performed at each time step from the minimization of loss functions defined recursively by backward induction. The methodology is extended to variational inequalities arising in optimal stopping problems. We analyze the convergence of the deep learning schemes and provide error estimates in terms of the universal approximation of neural networks. Numerical results show that our algorithms give very good results till dimension 50 (and certainly above), for both PDEs and variational inequalities problems. For the PDEs resolution, our results are very similar to those obtained by the recent method in \cite{weinan2017deep} when the latter converges to the right solution or does not diverge. Numerical tests indicate that the proposed methods are not stuck in poor local minimaas it can be the case with the algorithm designed in \cite{weinan2017deep}, and no divergence is experienced. The only limitation seems to be due to the inability of the considered deep neural networks to represent a solution with a too complex structure in high dimension.

Deep neural networks algorithms for stochastic control problems on finite horizon, Part 2: numerical applications

Dec 13, 2018

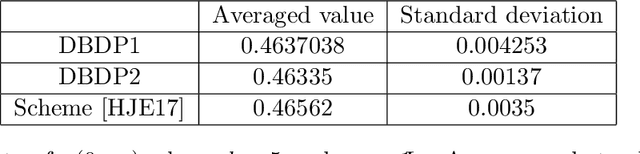

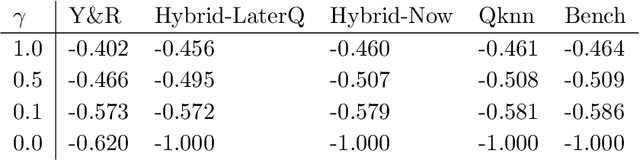

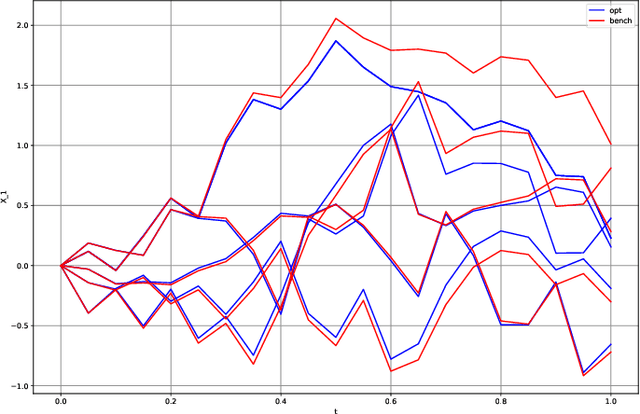

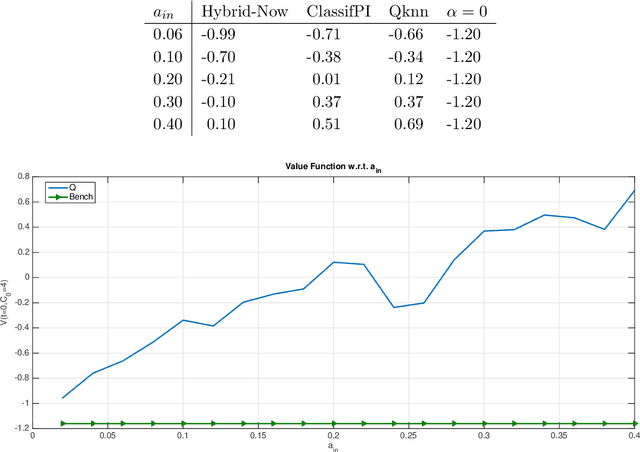

This paper presents several numerical applications of deep learning-based algorithms that have been analyzed in [11]. Numerical and comparative tests using TensorFlow illustrate the performance of our different algorithms, namely control learning by performance iteration (algorithms NNcontPI and ClassifPI), control learning by hybrid iteration (algorithms Hybrid-Now and Hybrid-LaterQ), on the 100-dimensional nonlinear PDEs examples from [6] and on quadratic Backward Stochastic Differential equations as in [5]. We also provide numerical results for an option hedging problem in finance, and energy storage problems arising in the valuation of gas storage and in microgrid management.

Deep neural networks algorithms for stochastic control problems on finite horizon, part I: convergence analysis

Dec 11, 2018

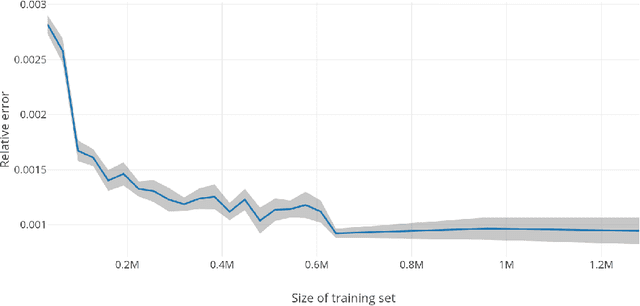

This paper develops algorithms for high-dimensional stochastic control problems based on deep learning and dynamic programming (DP). Differently from the classical approximate DP approach, we first approximate the optimal policy by means of neural networks in the spirit of deep reinforcement learning, and then the value function by Monte Carlo regression. This is achieved in the DP recursion by performance or hybrid iteration, and regress now or later/quantization methods from numerical probabilities. We provide a theoretical justification of these algorithms. Consistency and rate of convergence for the control and value function estimates are analyzed and expressed in terms of the universal approximation error of the neural networks. Numerical results on various applications are presented in a companion paper [2] and illustrate the performance of our algorithms.