Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeUsing Deep Learning for price prediction by exploiting stationary limit order book features

Oct 23, 2018

The recent surge in Deep Learning (DL) research of the past decade has successfully provided solutions to many difficult problems. The field of quantitative analysis has been slowly adapting the new methods to its problems, but due to problems such as the non-stationary nature of financial data, significant challenges must be overcome before DL is fully utilized. In this work a new method to construct stationary features, that allows DL models to be applied effectively, is proposed. These features are thoroughly tested on the task of predicting mid price movements of the Limit Order Book. Several DL models are evaluated, such as recurrent Long Short Term Memory (LSTM) networks and Convolutional Neural Networks (CNN). Finally a novel model that combines the ability of CNNs to extract useful features and the ability of LSTMs' to analyze time series, is proposed and evaluated. The combined model is able to outperform the individual LSTM and CNN models in the prediction horizons that are tested.

Machine Learning for Forecasting Mid Price Movement using Limit Order Book Data

Sep 19, 2018

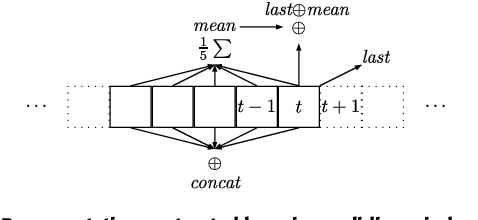

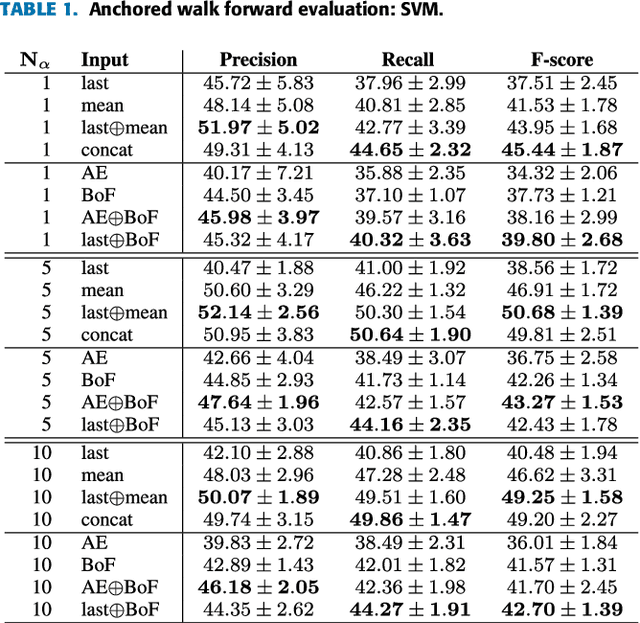

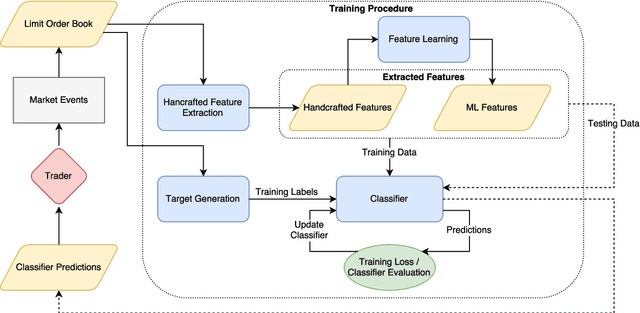

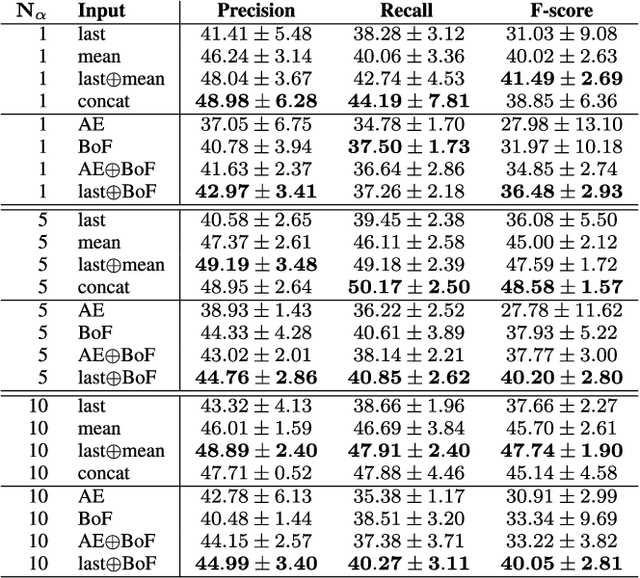

Forecasting the movements of stock prices is one the most challenging problems in financial markets analysis. In this paper, we use Machine Learning (ML) algorithms for the prediction of future price movements using limit order book data. Two different sets of features are combined and evaluated: handcrafted features based on the raw order book data and features extracted by ML algorithms, resulting in feature vectors with highly variant dimensionalities. Three classifiers are evaluated using combinations of these sets of features on two different evaluation setups and three prediction scenarios. Even though the large scale and high frequency nature of the limit order book poses several challenges, the scope of the conducted experiments and the significance of the experimental results indicate that Machine Learning highly befits this task carving the path towards future research in this field.