Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeJoint Online Learning and Decision-making via Dual Mirror Descent

Apr 20, 2021

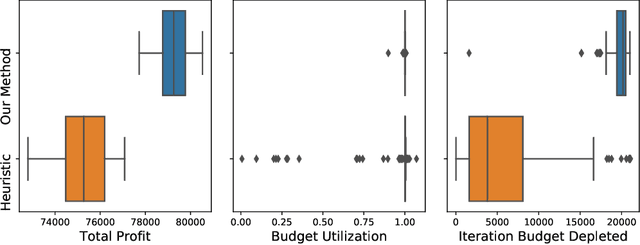

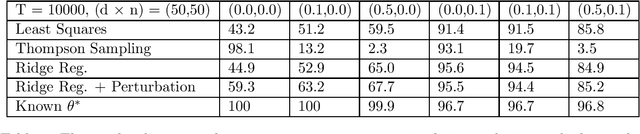

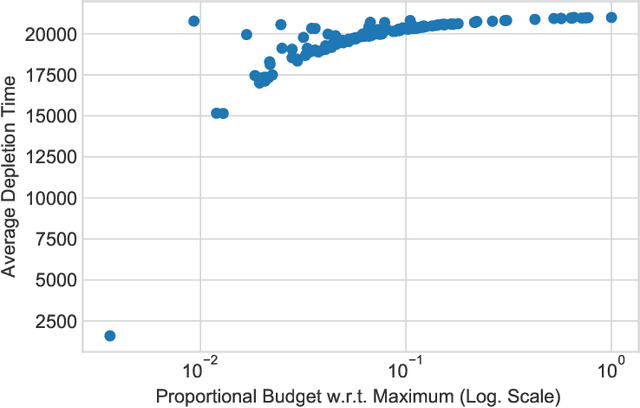

We consider an online revenue maximization problem over a finite time horizon subject to lower and upper bounds on cost. At each period, an agent receives a context vector sampled i.i.d. from an unknown distribution and needs to make a decision adaptively. The revenue and cost functions depend on the context vector as well as some fixed but possibly unknown parameter vector to be learned. We propose a novel offline benchmark and a new algorithm that mixes an online dual mirror descent scheme with a generic parameter learning process. When the parameter vector is known, we demonstrate an $O(\sqrt{T})$ regret result as well an $O(\sqrt{T})$ bound on the possible constraint violations. When the parameter is not known and must be learned, we demonstrate that the regret and constraint violations are the sums of the previous $O(\sqrt{T})$ terms plus terms that directly depend on the convergence of the learning process.

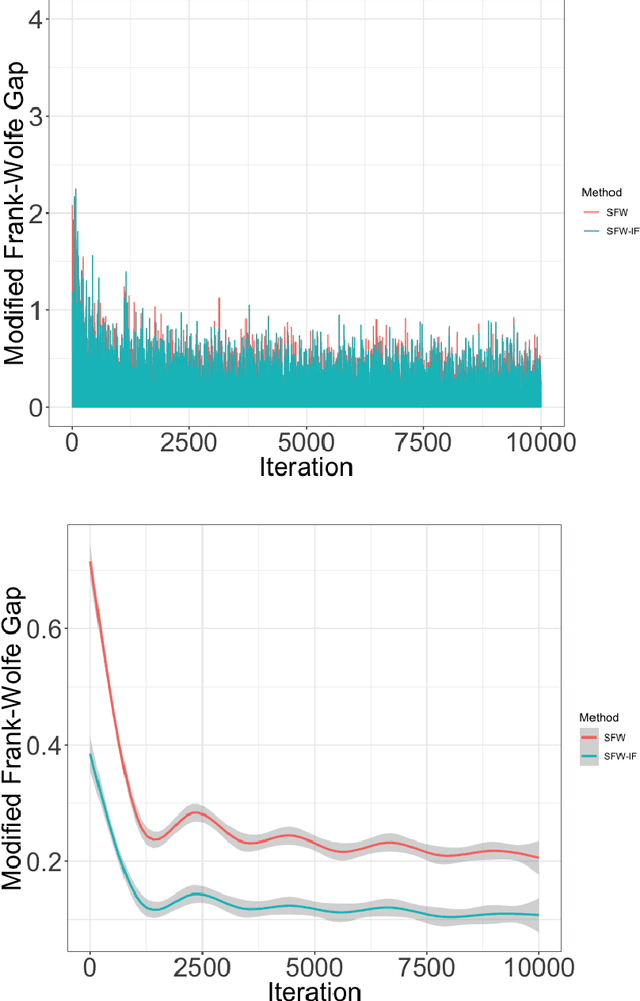

Stochastic In-Face Frank-Wolfe Methods for Non-Convex Optimization and Sparse Neural Network Training

Jun 09, 2019

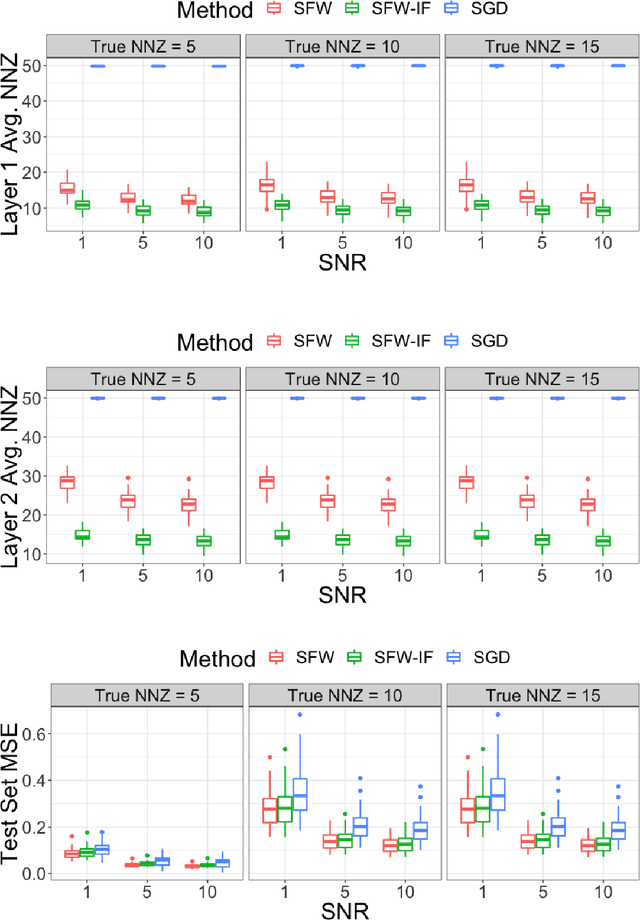

The Frank-Wolfe method and its extensions are well-suited for delivering solutions with desirable structural properties, such as sparsity or low-rank structure. We introduce a new variant of the Frank-Wolfe method that combines Frank-Wolfe steps and steepest descent steps, as well as a novel modification of the "Frank-Wolfe gap" to measure convergence in the non-convex case. We further extend this method to incorporate in-face directions for preserving structured solutions as well as block coordinate steps, and we demonstrate computational guarantees in terms of the modified Frank-Wolfe gap for all of these variants. We are particularly motivated by the application of this methodology to the training of neural networks with sparse properties, and we apply our block coordinate method to the problem of $\ell_1$ regularized neural network training. We present the results of several numerical experiments on both artificial and real datasets demonstrating significant improvements of our method in training sparse neural networks.