Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeJoint Online Learning and Decision-making via Dual Mirror Descent

Paper and Code

Apr 20, 2021

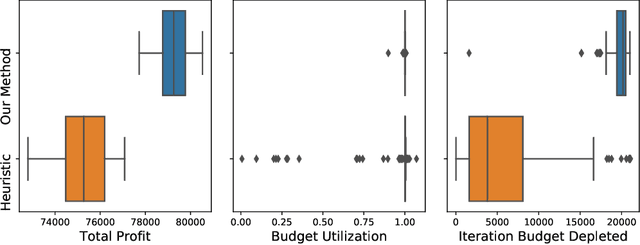

We consider an online revenue maximization problem over a finite time horizon subject to lower and upper bounds on cost. At each period, an agent receives a context vector sampled i.i.d. from an unknown distribution and needs to make a decision adaptively. The revenue and cost functions depend on the context vector as well as some fixed but possibly unknown parameter vector to be learned. We propose a novel offline benchmark and a new algorithm that mixes an online dual mirror descent scheme with a generic parameter learning process. When the parameter vector is known, we demonstrate an $O(\sqrt{T})$ regret result as well an $O(\sqrt{T})$ bound on the possible constraint violations. When the parameter is not known and must be learned, we demonstrate that the regret and constraint violations are the sums of the previous $O(\sqrt{T})$ terms plus terms that directly depend on the convergence of the learning process.