Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeDeepFolio: Convolutional Neural Networks for Portfolios with Limit Order Book Data

Aug 27, 2020

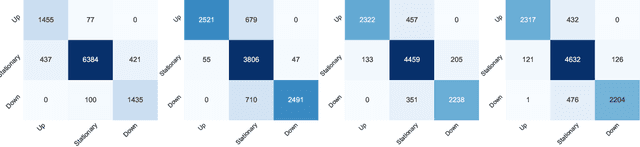

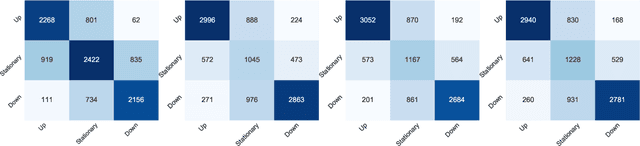

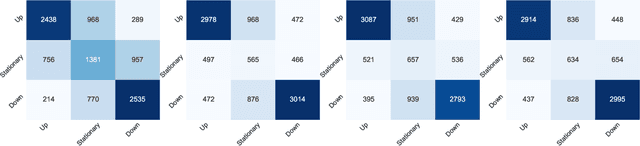

This work proposes DeepFolio, a new model for deep portfolio management based on data from limit order books (LOB). DeepFolio solves problems found in the state-of-the-art for LOB data to predict price movements. Our evaluation consists of two scenarios using a large dataset of millions of time series. The improvements deliver superior results both in cases of abundant as well as scarce data. The experiments show that DeepFolio outperforms the state-of-the-art on the benchmark FI-2010 LOB. Further, we use DeepFolio for optimal portfolio allocation of crypto-assets with rebalancing. For this purpose, we use two loss-functions - Sharpe ratio loss and minimum volatility risk. We show that DeepFolio outperforms widely used portfolio allocation techniques in the literature.