Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeTransformation Models in High-Dimensions

Paper and Code

Dec 20, 2017

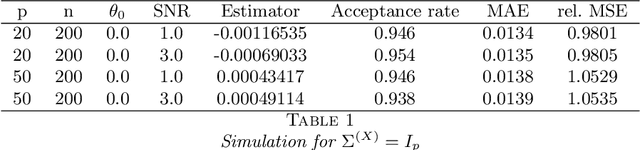

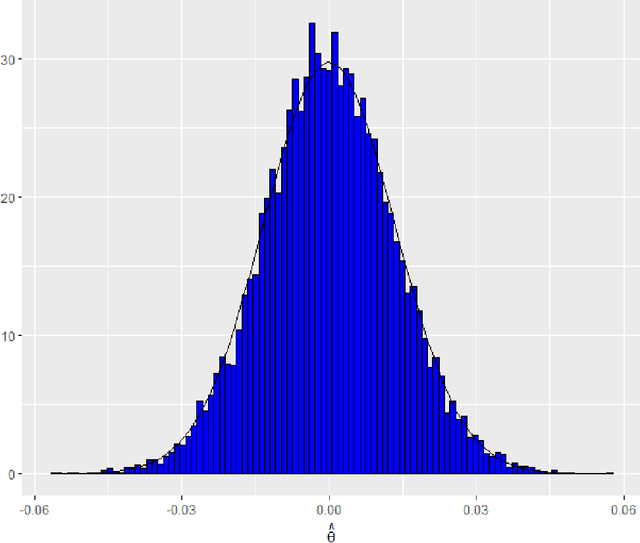

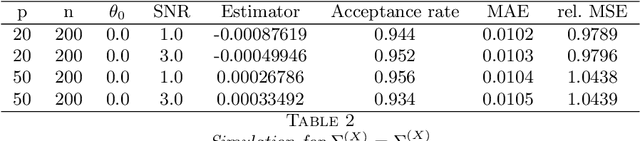

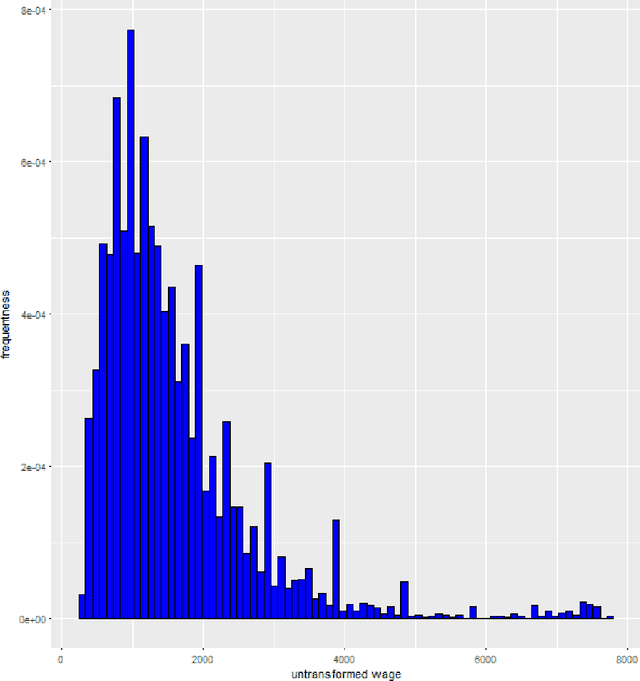

Transformation models are a very important tool for applied statisticians and econometricians. In many applications, the dependent variable is transformed so that homogeneity or normal distribution of the error holds. In this paper, we analyze transformation models in a high-dimensional setting, where the set of potential covariates is large. We propose an estimator for the transformation parameter and we show that it is asymptotically normally distributed using an orthogonalized moment condition where the nuisance functions depend on the target parameter. In a simulation study, we show that the proposed estimator works well in small samples. A common practice in labor economics is to transform wage with the log-function. In this study, we test if this transformation holds in CPS data from the United States.