Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeTesting for Conditional Mean Independence with Covariates through Martingale Difference Divergence

Paper and Code

May 17, 2018

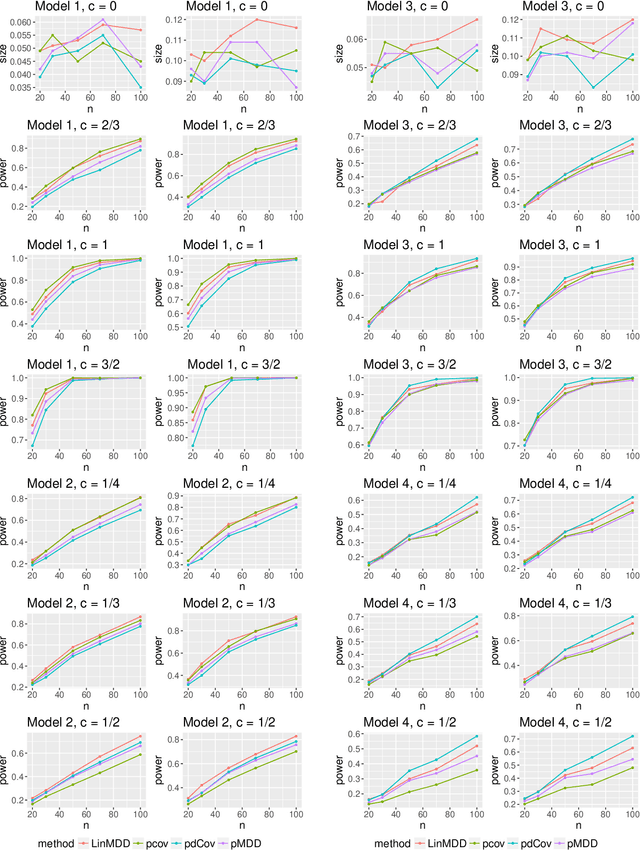

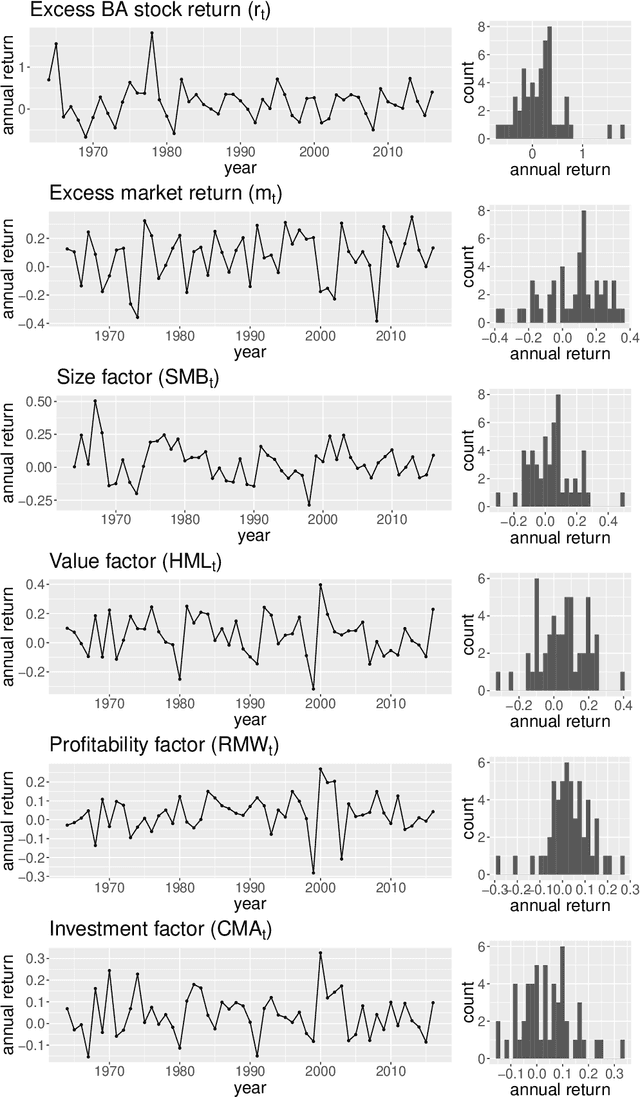

As a crucial problem in statistics is to decide whether additional variables are needed in a regression model. We propose a new multivariate test to investigate the conditional mean independence of Y given X conditioning on some known effect Z, i.e., E(Y|X, Z) = E(Y|Z). Assuming that E(Y|Z) and Z are linearly related, we reformulate an equivalent notion of conditional mean independence through transformation, which is approximated in practice. We apply the martingale difference divergence (Shao and Zhang, 2014) to measure conditional mean dependence, and show that the estimation error from approximation is negligible, as it has no impact on the asymptotic distribution of the test statistic under some regularity assumptions. The implementation of our test is demonstrated by both simulations and a financial data example.