Get our free extension to see links to code for papers anywhere online!Free add-on: code for papers everywhere!Free add-on: See code for papers anywhere!

Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeSome Developments in Clustering Analysis on Stochastic Processes

Paper and Code

Aug 05, 2019

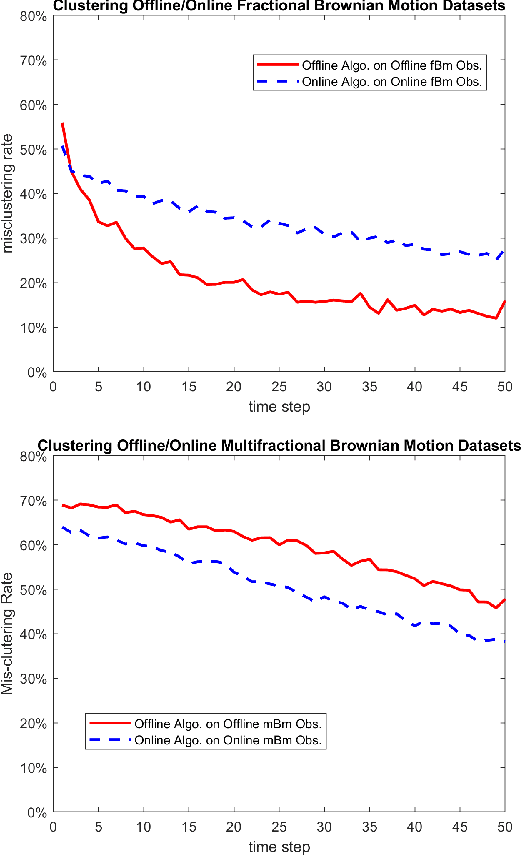

We review some developments on clustering stochastic processes and come with the conclusion that asymptotically consistent clustering algorithms can be obtained when the processes are ergodic and the dissimilarity measure satisfies the triangle inequality. Examples are provided when the processes are distribution ergodic, covariance ergodic and locally asymptotically self-similar, respectively.

View paper on