Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeRisk Management via Anomaly Circumvent: Mnemonic Deep Learning for Midterm Stock Prediction

Paper and Code

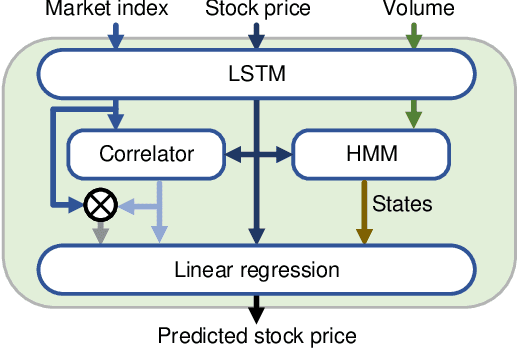

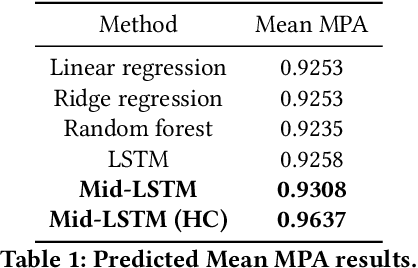

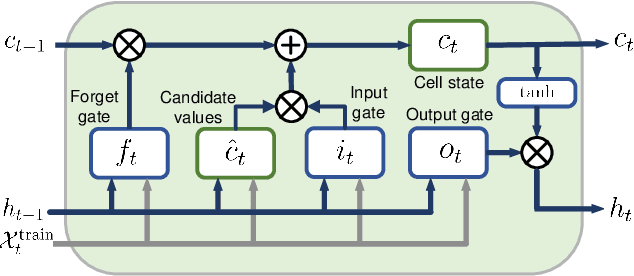

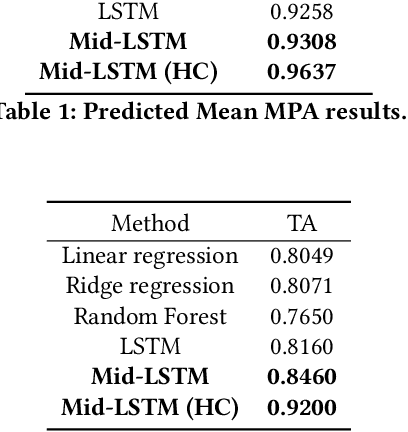

Midterm stock price prediction is crucial for value investments in the stock market. However, most deep learning models are essentially short-term and applying them to midterm predictions encounters large cumulative errors because they cannot avoid anomalies. In this paper, we propose a novel deep neural network Mid-LSTM for midterm stock prediction, which incorporates the market trend as hidden states. First, based on the autoregressive moving average model (ARMA), a midterm ARMA is formulated by taking into consideration both hidden states and the capital asset pricing model. Then, a midterm LSTM-based deep neural network is designed, which consists of three components: LSTM, hidden Markov model and linear regression networks. The proposed Mid-LSTM can avoid anomalies to reduce large prediction errors, and has good explanatory effects on the factors affecting stock prices. Extensive experiments on S&P 500 stocks show that (i) the proposed Mid-LSTM achieves 2-4% improvement in prediction accuracy, and (ii) in portfolio allocation investment, we achieve up to 120.16% annual return and 2.99 average Sharpe ratio.