Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgePredicting Sparse Clients' Actions with CPOPT-Net in the Banking Environment

Paper and Code

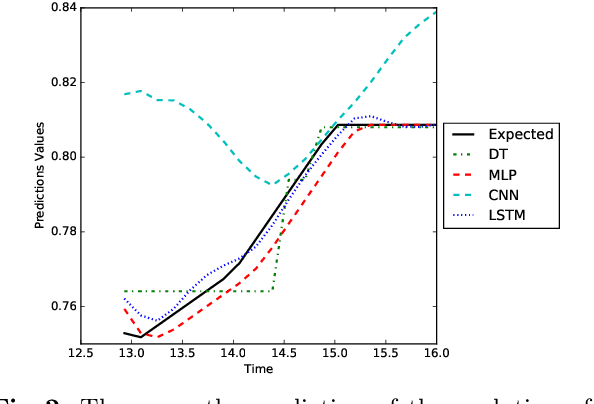

The digital revolution of the banking system with evolving European regulations have pushed the major banking actors to innovate by a newly use of their clients' digital information. Given highly sparse client activities, we propose CPOPT-Net, an algorithm that combines the CP canonical tensor decomposition, a multidimensional matrix decomposition that factorizes a tensor as the sum of rank-one tensors, and neural networks. CPOPT-Net removes efficiently sparse information with a gradient-based resolution while relying on neural networks for time series predictions. Our experiments show that CPOPT-Net is capable to perform accurate predictions of the clients' actions in the context of personalized recommendation. CPOPT-Net is the first algorithm to use non-linear conjugate gradient tensor resolution with neural networks to propose predictions of financial activities on a public data set.