Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeOSTSC: Over Sampling for Time Series Classification in R

Paper and Code

Nov 27, 2017

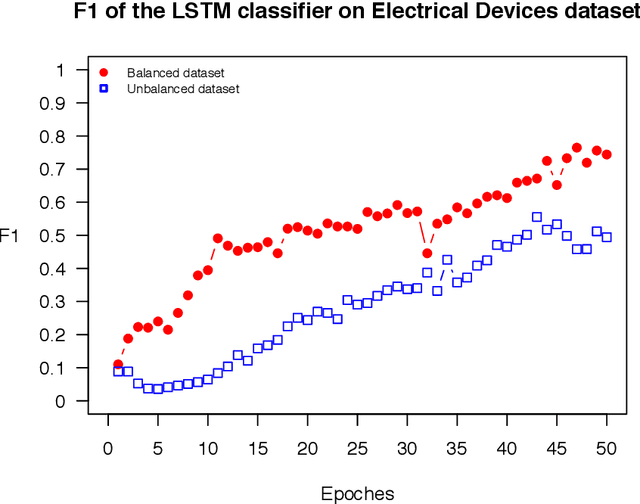

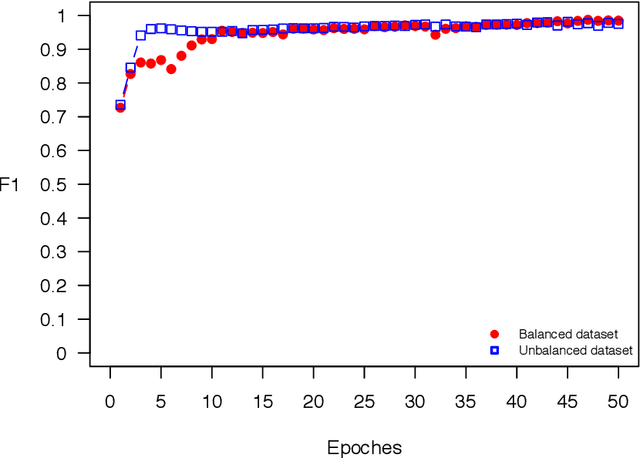

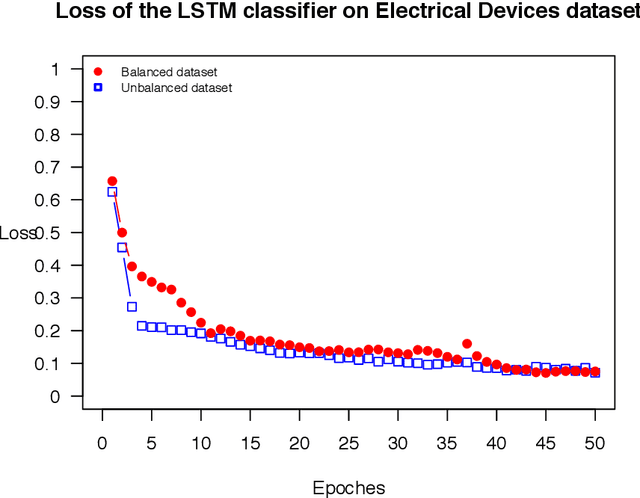

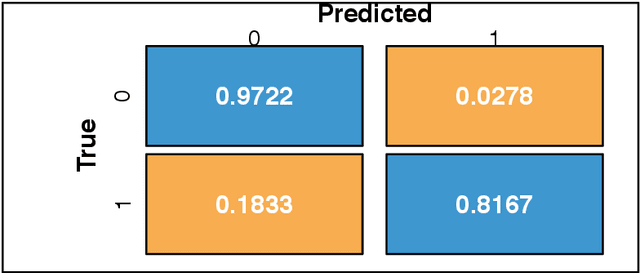

The OSTSC package is a powerful oversampling approach for classifying univariant, but multinomial time series data in R. This article provides a brief overview of the oversampling methodology implemented by the package. A tutorial of the OSTSC package is provided. We begin by providing three test cases for the user to quickly validate the functionality in the package. To demonstrate the performance impact of OSTSC, we then provide two medium size imbalanced time series datasets. Each example applies a TensorFlow implementation of a Long Short-Term Memory (LSTM) classifier - a type of a Recurrent Neural Network (RNN) classifier - to imbalanced time series. The classifier performance is compared with and without oversampling. Finally, larger versions of these two datasets are evaluated to demonstrate the scalability of the package. The examples demonstrate that the OSTSC package improves the performance of RNN classifiers applied to highly imbalanced time series data. In particular, OSTSC is observed to increase the AUC of LSTM from 0.543 to 0.784 on a high frequency trading dataset consisting of 30,000 time series observations.