Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeOff-policy estimation of linear functionals: Non-asymptotic theory for semi-parametric efficiency

Paper and Code

Sep 26, 2022

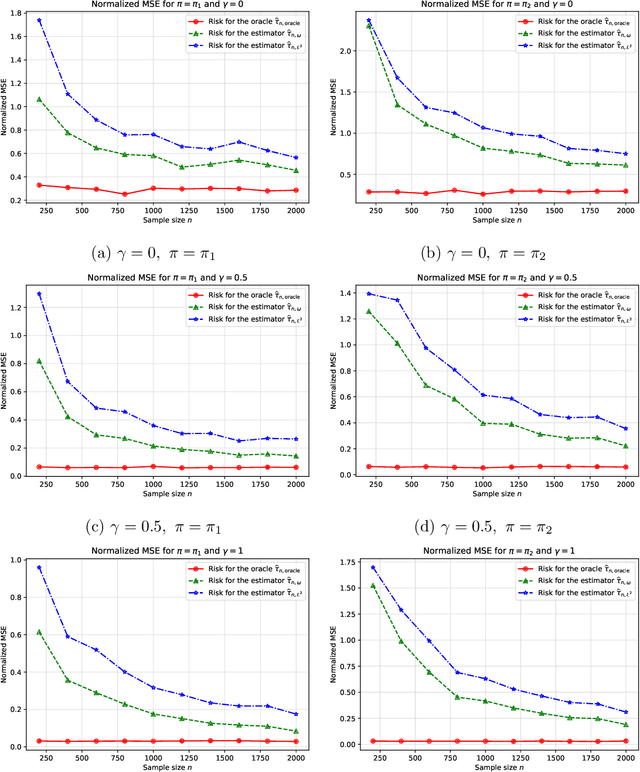

The problem of estimating a linear functional based on observational data is canonical in both the causal inference and bandit literatures. We analyze a broad class of two-stage procedures that first estimate the treatment effect function, and then use this quantity to estimate the linear functional. We prove non-asymptotic upper bounds on the mean-squared error of such procedures: these bounds reveal that in order to obtain non-asymptotically optimal procedures, the error in estimating the treatment effect should be minimized in a certain weighted $L^2$-norm. We analyze a two-stage procedure based on constrained regression in this weighted norm, and establish its instance-dependent optimality in finite samples via matching non-asymptotic local minimax lower bounds. These results show that the optimal non-asymptotic risk, in addition to depending on the asymptotically efficient variance, depends on the weighted norm distance between the true outcome function and its approximation by the richest function class supported by the sample size.