Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeNon-parametric Probabilistic Time Series Forecasting via Innovations Representation

Paper and Code

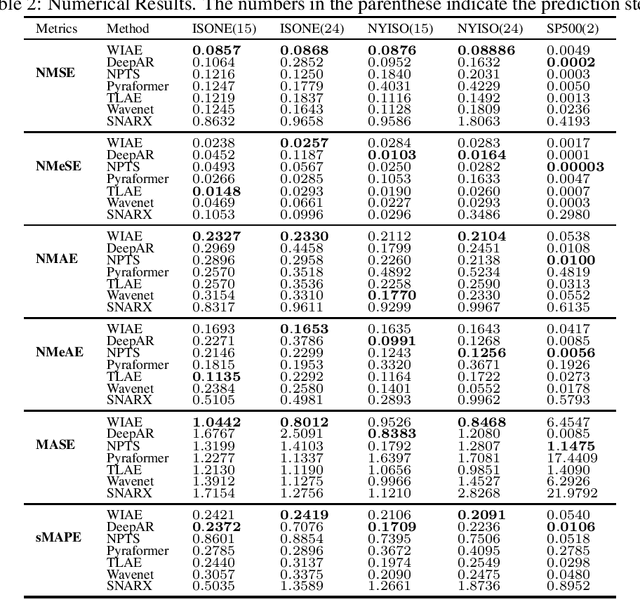

Probabilistic time series forecasting predicts the conditional probability distributions of the time series at a future time given past realizations. Such techniques are critical in risk-based decision-making and planning under uncertainties. Existing approaches are primarily based on parametric or semi-parametric time-series models that are restrictive, difficult to validate, and challenging to adapt to varying conditions. This paper proposes a nonparametric method based on the classic notion of {\em innovations} pioneered by Norbert Wiener and Gopinath Kallianpur that causally transforms a nonparametric random process to an independent and identical uniformly distributed {\em innovations process}. We present a machine-learning architecture and a learning algorithm that circumvent two limitations of the original Wiener-Kallianpur innovations representation: (i) the need for known probability distributions of the time series and (ii) the existence of a causal decoder that reproduces the original time series from the innovations representation. We develop a deep-learning approach and a Monte Carlo sampling technique to obtain a generative model for the predicted conditional probability distribution of the time series based on a weak notion of Wiener-Kallianpur innovations representation. The efficacy of the proposed probabilistic forecasting technique is demonstrated on a variety of electricity price datasets, showing marked improvement over leading benchmarks of probabilistic forecasting techniques.