Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeNo-Regret Learning in Partially-Informed Auctions

Paper and Code

Feb 22, 2022

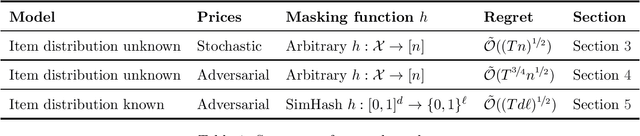

Auctions with partially-revealed information about items are broadly employed in real-world applications, but the underlying mechanisms have limited theoretical support. In this work, we study a machine learning formulation of these types of mechanisms, presenting algorithms that are no-regret from the buyer's perspective. Specifically, a buyer who wishes to maximize his utility interacts repeatedly with a platform over a series of $T$ rounds. In each round, a new item is drawn from an unknown distribution and the platform publishes a price together with incomplete, "masked" information about the item. The buyer then decides whether to purchase the item. We formalize this problem as an online learning task where the goal is to have low regret with respect to a myopic oracle that has perfect knowledge of the distribution over items and the seller's masking function. When the distribution over items is known to the buyer and the mask is a SimHash function mapping $\mathbb{R}^d$ to $\{0,1\}^{\ell}$, our algorithm has regret $\tilde {\mathcal{O}}((Td\ell)^{\frac{1}{2}})$. In a fully agnostic setting when the mask is an arbitrary function mapping to a set of size $n$, our algorithm has regret $\tilde {\mathcal{O}}(T^{\frac{3}{4}}n^{\frac{1}{2}})$. Finally, when the prices are stochastic, the algorithm has regret $\tilde {\mathcal{O}}((Tn)^{\frac{1}{2}})$.