Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeMixSeq: Connecting Macroscopic Time Series Forecasting with Microscopic Time Series Data

Paper and Code

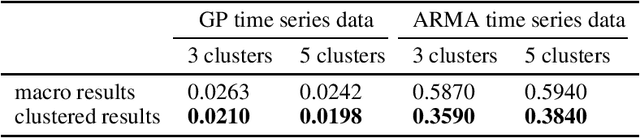

Time series forecasting is widely used in business intelligence, e.g., forecast stock market price, sales, and help the analysis of data trend. Most time series of interest are macroscopic time series that are aggregated from microscopic data. However, instead of directly modeling the macroscopic time series, rare literature studied the forecasting of macroscopic time series by leveraging data on the microscopic level. In this paper, we assume that the microscopic time series follow some unknown mixture probabilistic distributions. We theoretically show that as we identify the ground truth latent mixture components, the estimation of time series from each component could be improved because of lower variance, thus benefitting the estimation of macroscopic time series as well. Inspired by the power of Seq2seq and its variants on the modeling of time series data, we propose Mixture of Seq2seq (MixSeq), an end2end mixture model to cluster microscopic time series, where all the components come from a family of Seq2seq models parameterized by different parameters. Extensive experiments on both synthetic and real-world data show the superiority of our approach.