Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeLearning the Truth From Only One Side of the Story

Paper and Code

Jun 08, 2020

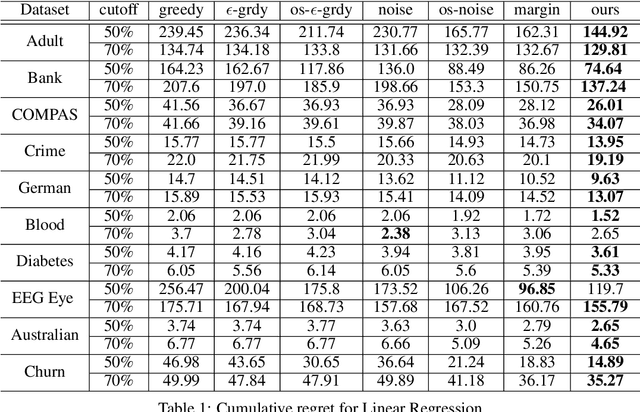

Learning under one-sided feedback (i.e., where examples arrive in an online fashion and the learner only sees the labels for examples it predicted positively on) is a fundamental problem in machine learning -- applications include lending and recommendation systems. Despite this, there has been surprisingly little progress made in ways to mitigate the effects of the sampling bias that arises. We focus on generalized linear models and show that without adjusting for this sampling bias, the model may converge sub-optimally or even fail to converge to the optimal solution. We propose an adaptive Upper Confidence Bound approach that comes with rigorous regret guarantees and we show that it outperforms several existing methods experimentally. Our method leverages uncertainty estimation techniques for generalized linear models to more efficiently explore uncertain areas than existing approaches which explore randomly.