Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeLearning Against Distributional Uncertainty: On the Trade-off Between Robustness and Specificity

Paper and Code

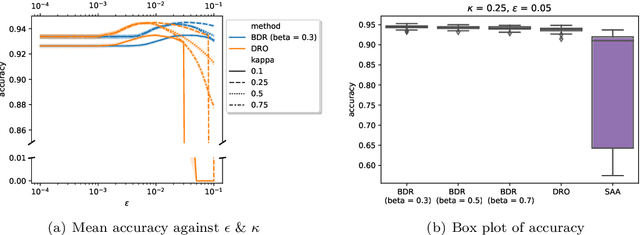

Trustworthy machine learning aims at combating distributional uncertainties in training data distributions compared to population distributions. Typical treatment frameworks include the Bayesian approach, (min-max) distributionally robust optimization (DRO), and regularization. However, two issues have to be raised: 1) All these methods are biased estimators of the true optimal cost; 2) the prior distribution in the Bayesian method, the radius of the distributional ball in the DRO method, and the regularizer in the regularization method are difficult to specify. This paper studies a new framework that unifies the three approaches and that addresses the two challenges mentioned above. The asymptotic properties (e.g., consistency and asymptotic normalities), non-asymptotic properties (e.g., unbiasedness and generalization error bound), and a Monte--Carlo-based solution method of the proposed model are studied. The new model reveals the trade-off between the robustness to the unseen data and the specificity to the training data.