Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeInventory Control Involving Unknown Demand of Discrete Nonperishable Items - Analysis of a Newsvendor-based Policy

Paper and Code

Oct 22, 2015

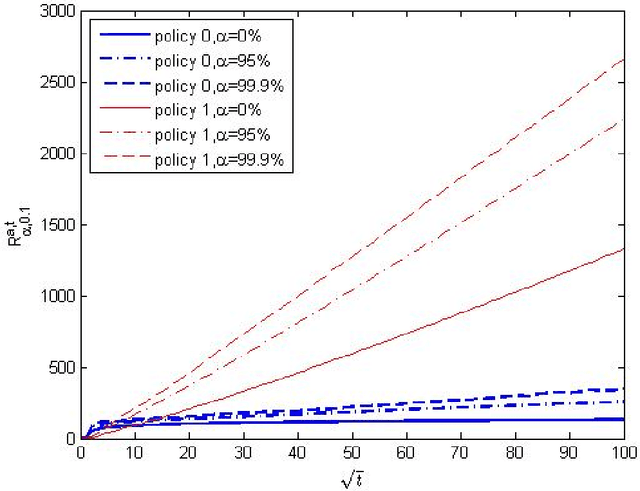

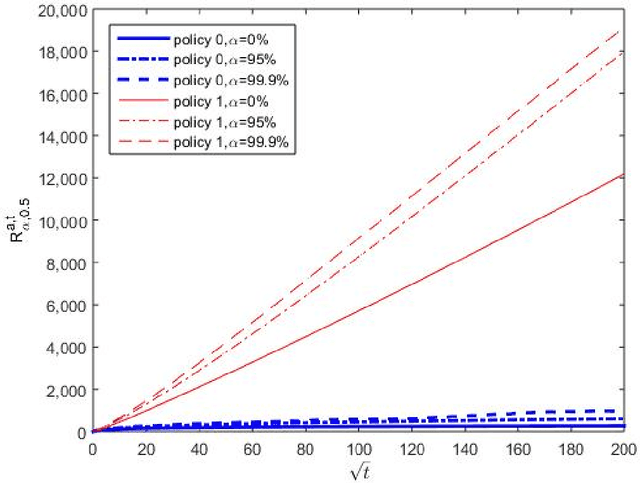

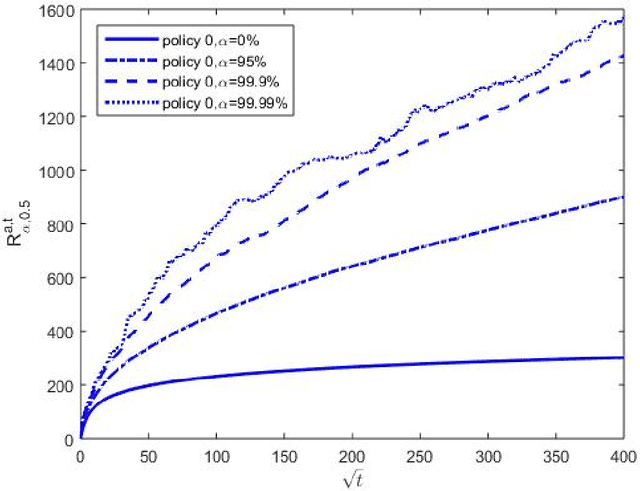

Inventory control with unknown demand distribution is considered, with emphasis placed on the case involving discrete nonperishable items. We focus on an adaptive policy which in every period uses, as much as possible, the optimal newsvendor ordering quantity for the empirical distribution learned up to that period. The policy is assessed using the regret criterion, which measures the price paid for ambiguity on demand distribution over $T$ periods. When there are guarantees on the latter's separation from the critical newsvendor parameter $\beta=b/(h+b)$, a constant upper bound on regret can be found. Without any prior information on the demand distribution, we show that the regret does not grow faster than the rate $T^{1/2+\epsilon}$ for any $\epsilon>0$. In view of a known lower bound, this is almost the best one could hope for. Simulation studies involving this along with other policies are also conducted.