Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeInertial Regularization and Selection (IRS): Sequential Regression in High-Dimension and Sparsity

Paper and Code

Jan 10, 2017

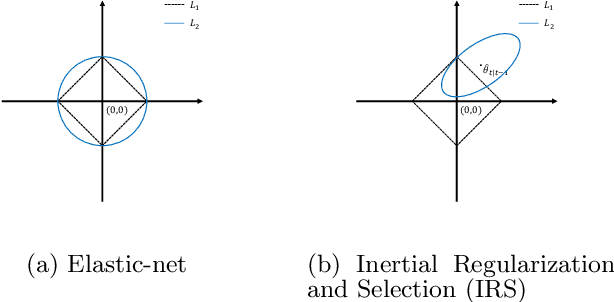

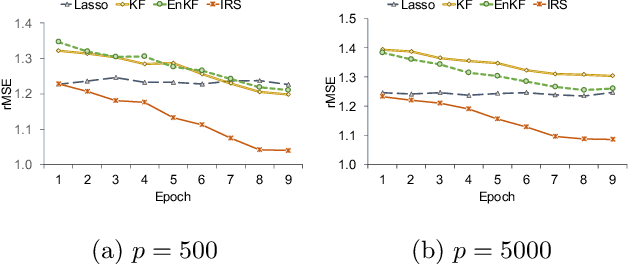

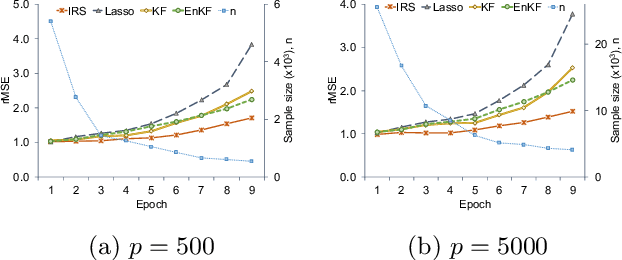

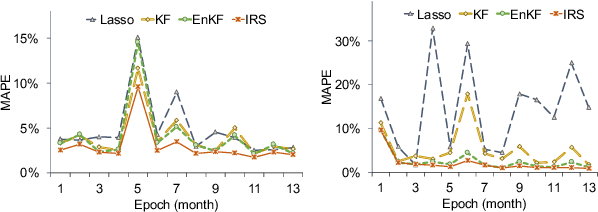

In this paper, we develop a new sequential regression modeling approach for data streams. Data streams are commonly found around us, e.g in a retail enterprise sales data is continuously collected every day. A demand forecasting model is an important outcome from the data that needs to be continuously updated with the new incoming data. The main challenge in such modeling arises when there is a) high dimensional and sparsity, b) need for an adaptive use of prior knowledge, and/or c) structural changes in the system. The proposed approach addresses these challenges by incorporating an adaptive L1-penalty and inertia terms in the loss function, and thus called Inertial Regularization and Selection (IRS). The former term performs model selection to handle the first challenge while the latter is shown to address the last two challenges. A recursive estimation algorithm is developed, and shown to outperform the commonly used state-space models, such as Kalman Filters, in experimental studies and real data.