Get our free extension to see links to code for papers anywhere online!Free add-on: code for papers everywhere!Free add-on: See code for papers anywhere!

Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeGraphical Models for Financial Time Series and Portfolio Selection

Paper and Code

Jan 22, 2021

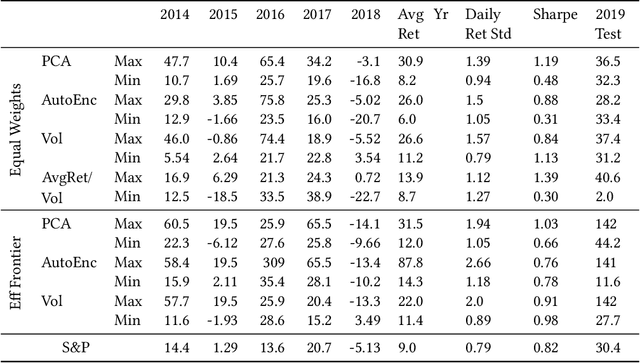

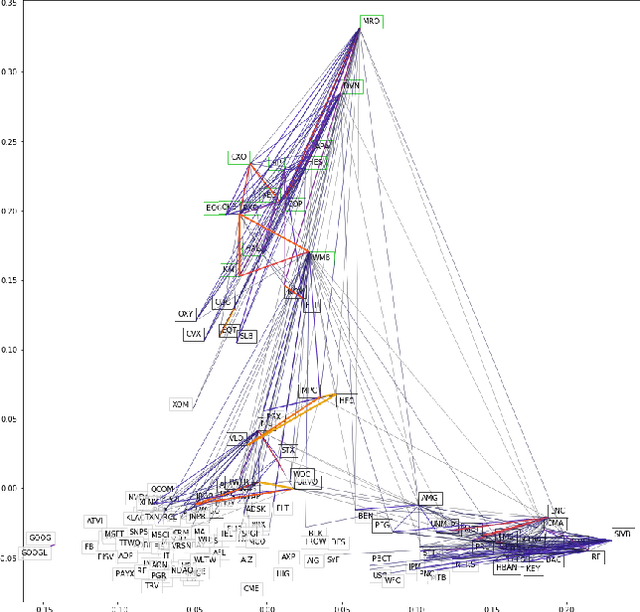

We examine a variety of graphical models to construct optimal portfolios. Graphical models such as PCA-KMeans, autoencoders, dynamic clustering, and structural learning can capture the time varying patterns in the covariance matrix and allow the creation of an optimal and robust portfolio. We compared the resulting portfolios from the different models with baseline methods. In many cases our graphical strategies generated steadily increasing returns with low risk and outgrew the S&P 500 index. This work suggests that graphical models can effectively learn the temporal dependencies in time series data and are proved useful in asset management.

* Published at ACM International Conference on AI in Finance (ICAIF

'20)

View paper on