Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeGaussian Process Conditional Copulas with Applications to Financial Time Series

Paper and Code

Jul 01, 2013

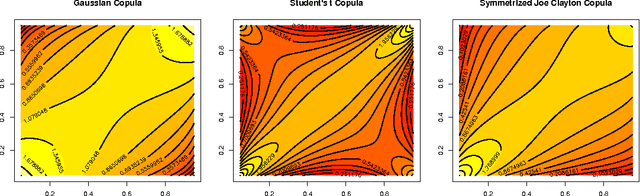

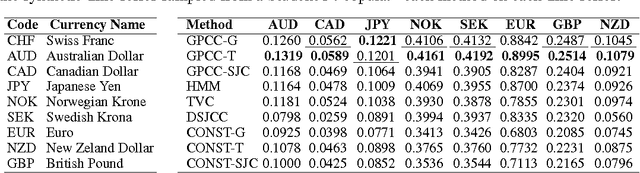

The estimation of dependencies between multiple variables is a central problem in the analysis of financial time series. A common approach is to express these dependencies in terms of a copula function. Typically the copula function is assumed to be constant but this may be inaccurate when there are covariates that could have a large influence on the dependence structure of the data. To account for this, a Bayesian framework for the estimation of conditional copulas is proposed. In this framework the parameters of a copula are non-linearly related to some arbitrary conditioning variables. We evaluate the ability of our method to predict time-varying dependencies on several equities and currencies and observe consistent performance gains compared to static copula models and other time-varying copula methods.