Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeFEUP at SemEval-2017 Task 5: Predicting Sentiment Polarity and Intensity with Financial Word Embeddings

Paper and Code

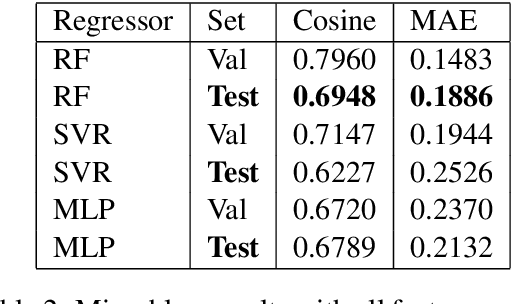

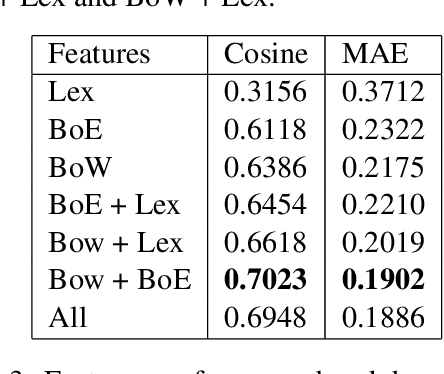

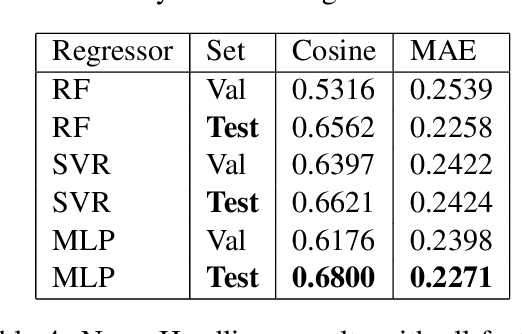

This paper presents the approach developed at the Faculty of Engineering of University of Porto, to participate in SemEval 2017, Task 5: Fine-grained Sentiment Analysis on Financial Microblogs and News. The task consisted in predicting a real continuous variable from -1.0 to +1.0 representing the polarity and intensity of sentiment concerning companies/stocks mentioned in short texts. We modeled the task as a regression analysis problem and combined traditional techniques such as pre-processing short texts, bag-of-words representations and lexical-based features with enhanced financial specific bag-of-embeddings. We used an external collection of tweets and news headlines mentioning companies/stocks from S\&P 500 to create financial word embeddings which are able to capture domain-specific syntactic and semantic similarities. The resulting approach obtained a cosine similarity score of 0.69 in sub-task 5.1 - Microblogs and 0.68 in sub-task 5.2 - News Headlines.