Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeDynamic treatment effects: high-dimensional inference under model misspecification

Paper and Code

Nov 12, 2021

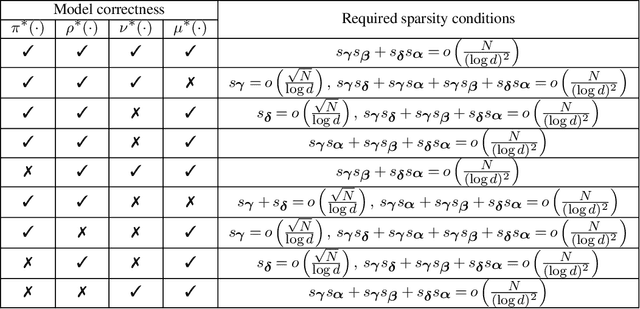

This paper considers the inference for heterogeneous treatment effects in dynamic settings that covariates and treatments are longitudinal. We focus on high-dimensional cases that the sample size, $N$, is potentially much larger than the covariate vector's dimension, $d$. The marginal structural mean models are considered. We propose a "sequential model doubly robust" estimator constructed based on "moment targeted" nuisance estimators. Such nuisance estimators are carefully designed through non-standard loss functions, reducing the bias resulting from potential model misspecifications. We achieve $\sqrt N$-inference even when model misspecification occurs. We only require one nuisance model to be correctly specified at each time spot. Such model correctness conditions are weaker than all the existing work, even containing the literature on low dimensions.