Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeDistribution-Free Model-Agnostic Regression Calibration via Nonparametric Methods

Paper and Code

May 20, 2023

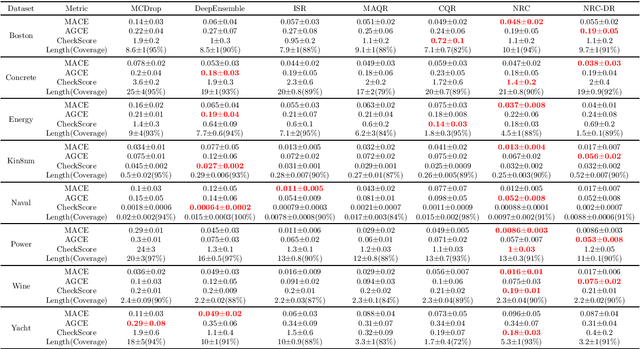

In this paper, we consider the uncertainty quantification problem for regression models. Specifically, we consider an individual calibration objective for characterizing the quantiles of the prediction model. While such an objective is well-motivated from downstream tasks such as newsvendor cost, the existing methods have been largely heuristic and lack of statistical guarantee in terms of individual calibration. We show via simple examples that the existing methods focusing on population-level calibration guarantees such as average calibration or sharpness can lead to harmful and unexpected results. We propose simple nonparametric calibration methods that are agnostic of the underlying prediction model and enjoy both computational efficiency and statistical consistency. Our approach enables a better understanding of the possibility of individual calibration, and we establish matching upper and lower bounds for the calibration error of our proposed methods. Technically, our analysis combines the nonparametric analysis with a covering number argument for parametric analysis, which advances the existing theoretical analyses in the literature of nonparametric density estimation and quantile bandit problems. Importantly, the nonparametric perspective sheds new theoretical insights into regression calibration in terms of the curse of dimensionality and reconciles the existing results on the impossibility of individual calibration. Numerical experiments show the advantage of such a simple approach under various metrics, and also under covariates shift. We hope our work provides a simple benchmark and a starting point of theoretical ground for future research on regression calibration.