Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeDepth-based pseudo-metrics between probability distributions

Paper and Code

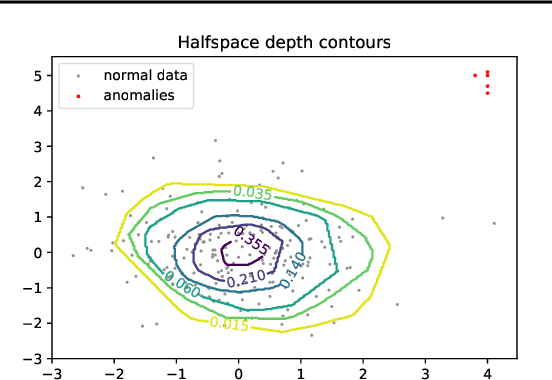

Data depth is a non parametric statistical tool that measures centrality of any element $x\in\mathbb{R}^d$ with respect to (w.r.t.) a probability distribution or a data set. It is a natural median-oriented extension of the cumulative distribution function (cdf) to the multivariate case. Consequently, its upper level sets -- the depth-trimmed regions -- give rise to a definition of multivariate quantiles. In this work, we propose two new pseudo-metrics between continuous probability measures based on data depth and its associated central regions. The first one is constructed as the Lp-distance between data depth w.r.t. each distribution while the second one relies on the Hausdorff distance between their quantile regions. It can further be seen as an original way to extend the one-dimensional formulae of the Wasserstein distance, which involves quantiles and cdfs, to the multivariate space. After discussing the properties of these pseudo-metrics and providing conditions under which they define a distance, we highlight similarities with the Wasserstein distance. Interestingly, the derived non-asymptotic bounds show that in contrast to the Wasserstein distance, the proposed pseudo-metrics do not suffer from the curse of dimensionality. Moreover, based on the support function of a convex body, we propose an efficient approximation possessing linear time complexity w.r.t. the size of the data set and its dimension. The quality of this approximation as well as the performance of the proposed approach are illustrated in experiments. Furthermore, by construction the regions-based pseudo-metric appears to be robust w.r.t. both outliers and heavy tails, a behavior witnessed in the numerical experiments.