Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeCross Cryptocurrency Relationship Mining for Bitcoin Price Prediction

Paper and Code

Apr 28, 2022

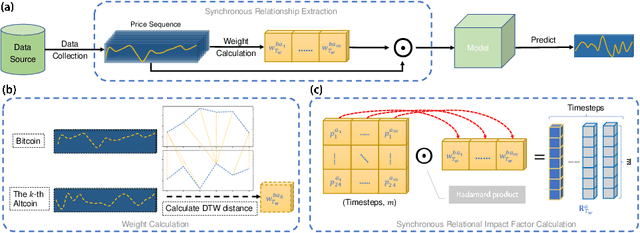

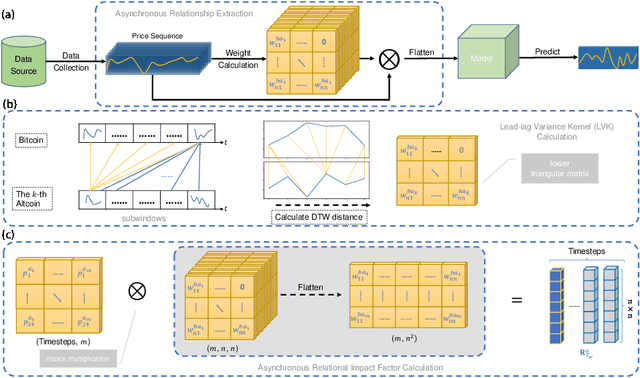

Blockchain finance has become a part of the world financial system, most typically manifested in the attention to the price of Bitcoin. However, a great deal of work is still limited to using technical indicators to capture Bitcoin price fluctuation, with little consideration of historical relationships and interactions between related cryptocurrencies. In this work, we propose a generic Cross-Cryptocurrency Relationship Mining module, named C2RM, which can effectively capture the synchronous and asynchronous impact factors between Bitcoin and related Altcoins. Specifically, we utilize the Dynamic Time Warping algorithm to extract the lead-lag relationship, yielding Lead-lag Variance Kernel, which will be used for aggregating the information of Altcoins to form relational impact factors. Comprehensive experimental results demonstrate that our C2RM can help existing price prediction methods achieve significant performance improvement, suggesting the effectiveness of Cross-Cryptocurrency interactions on benefitting Bitcoin price prediction.