Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeConvergence of policy gradient methods for finite-horizon stochastic linear-quadratic control problems

Paper and Code

Nov 01, 2022

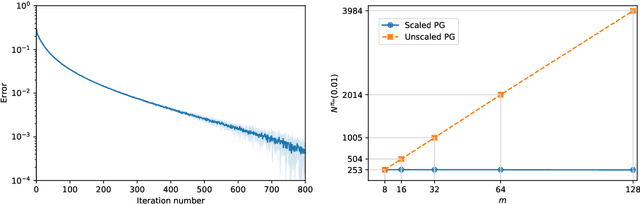

We study the global linear convergence of policy gradient (PG) methods for finite-horizon exploratory linear-quadratic control (LQC) problems. The setting includes stochastic LQC problems with indefinite costs and allows additional entropy regularisers in the objective. We consider a continuous-time Gaussian policy whose mean is linear in the state variable and whose covariance is state-independent. Contrary to discrete-time problems, the cost is noncoercive in the policy and not all descent directions lead to bounded iterates. We propose geometry-aware gradient descents for the mean and covariance of the policy using the Fisher geometry and the Bures-Wasserstein geometry, respectively. The policy iterates are shown to satisfy an a-priori bound, and converge globally to the optimal policy with a linear rate. We further propose a novel PG method with discrete-time policies. The algorithm leverages the continuous-time analysis, and achieves a robust linear convergence across different action frequencies. A numerical experiment confirms the convergence and robustness of the proposed algorithm.