Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeConservative Contextual Bandits: Beyond Linear Representations

Paper and Code

Dec 09, 2024

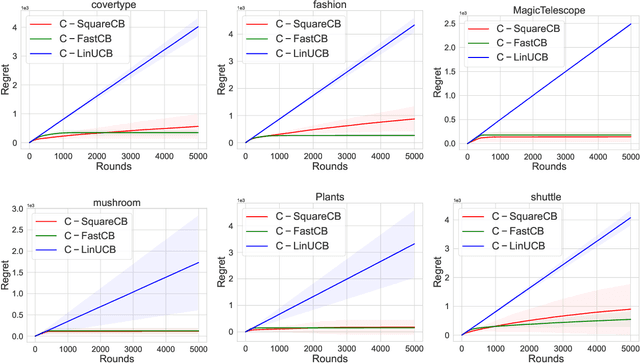

Conservative Contextual Bandits (CCBs) address safety in sequential decision making by requiring that an agent's policy, along with minimizing regret, also satisfies a safety constraint: the performance is not worse than a baseline policy (e.g., the policy that the company has in production) by more than $(1+\alpha)$ factor. Prior work developed UCB-style algorithms in the multi-armed [Wu et al., 2016] and contextual linear [Kazerouni et al., 2017] settings. However, in practice the cost of the arms is often a non-linear function, and therefore existing UCB algorithms are ineffective in such settings. In this paper, we consider CCBs beyond the linear case and develop two algorithms $\mathtt{C-SquareCB}$ and $\mathtt{C-FastCB}$, using Inverse Gap Weighting (IGW) based exploration and an online regression oracle. We show that the safety constraint is satisfied with high probability and that the regret of $\mathtt{C-SquareCB}$ is sub-linear in horizon $T$, while the regret of $\mathtt{C-FastCB}$ is first-order and is sub-linear in $L^*$, the cumulative loss of the optimal policy. Subsequently, we use a neural network for function approximation and online gradient descent as the regression oracle to provide $\tilde{O}(\sqrt{KT} + K/\alpha) $ and $\tilde{O}(\sqrt{KL^*} + K (1 + 1/\alpha))$ regret bounds, respectively. Finally, we demonstrate the efficacy of our algorithms on real-world data and show that they significantly outperform the existing baseline while maintaining the performance guarantee.