Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeConformal Prediction with Temporal Quantile Adjustments

Paper and Code

May 23, 2022

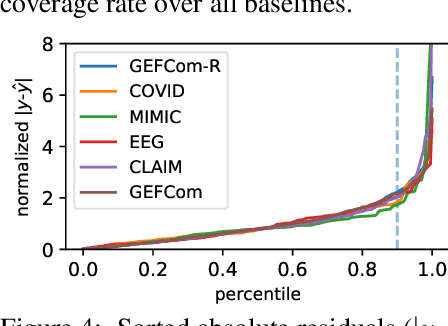

We develop Temporal Quantile Adjustment (TQA), a general method to construct efficient and valid prediction intervals (PIs) for regression on cross-sectional time series data. Such data is common in many domains, including econometrics and healthcare. A canonical example in healthcare is predicting patient outcomes using physiological time-series data, where a population of patients composes a cross-section. Reliable PI estimators in this setting must address two distinct notions of coverage: cross-sectional coverage across a cross-sectional slice, and longitudinal coverage along the temporal dimension for each time series. Recent works have explored adapting Conformal Prediction (CP) to obtain PIs in the time series context. However, none handles both notions of coverage simultaneously. CP methods typically query a pre-specified quantile from the distribution of nonconformity scores on a calibration set. TQA adjusts the quantile to query in CP at each time $t$, accounting for both cross-sectional and longitudinal coverage in a theoretically-grounded manner. The post-hoc nature of TQA facilitates its use as a general wrapper around any time series regression model. We validate TQA's performance through extensive experimentation: TQA generally obtains efficient PIs and improves longitudinal coverage while preserving cross-sectional coverage.