Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeBellman Conformal Inference: Calibrating Prediction Intervals For Time Series

Paper and Code

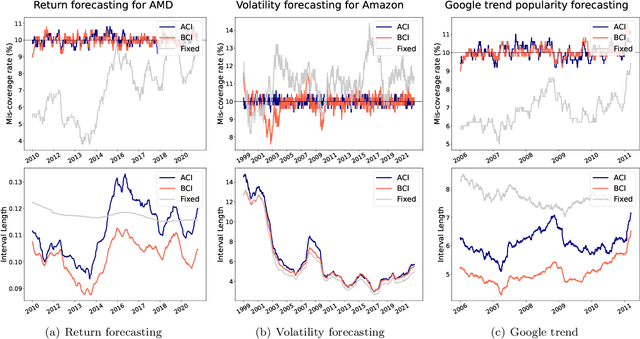

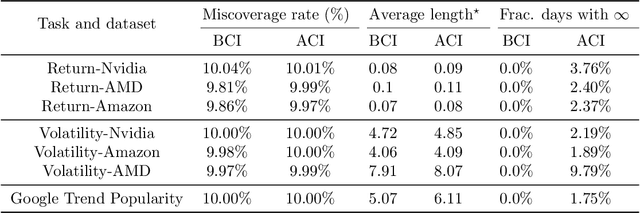

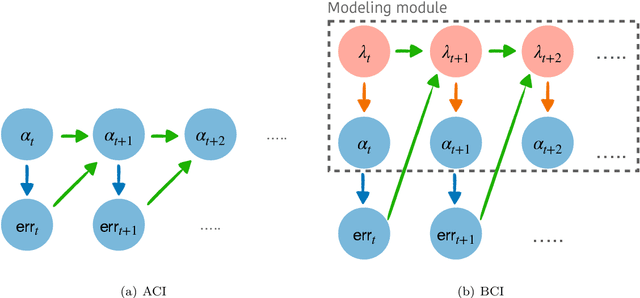

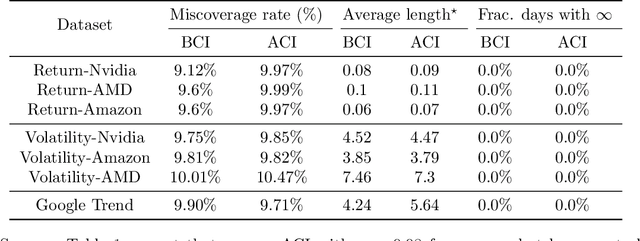

We introduce Bellman Conformal Inference (BCI), a framework that wraps around any time series forecasting models and provides approximately calibrated prediction intervals. Unlike existing methods, BCI is able to leverage multi-step ahead forecasts and explicitly optimize the average interval lengths by solving a one-dimensional stochastic control problem (SCP) at each time step. In particular, we use the dynamic programming algorithm to find the optimal policy for the SCP. We prove that BCI achieves long-term coverage under arbitrary distribution shifts and temporal dependence, even with poor multi-step ahead forecasts. We find empirically that BCI avoids uninformative intervals that have infinite lengths and generates substantially shorter prediction intervals in multiple applications when compared with existing methods.