Get our free extension to see links to code for papers anywhere online!Free add-on: code for papers everywhere!Free add-on: See code for papers anywhere!

Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeArbitrage-Free Implied Volatility Surface Generation with Variational Autoencoders

Paper and Code

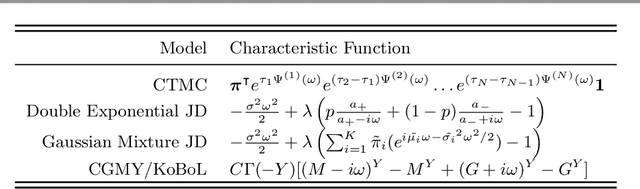

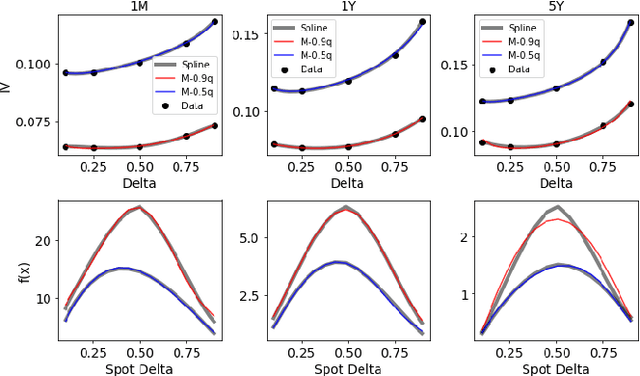

We propose a hybrid method for generating arbitrage-free implied volatility (IV) surfaces consistent with historical data by combining model-free Variational Autoencoders (VAEs) with continuous time stochastic differential equation (SDE) driven models. We focus on two classes of SDE models: regime switching models and L\'evy additive processes. By projecting historical surfaces onto the space of SDE model parameters, we obtain a distribution on the parameter subspace faithful to the data on which we then train a VAE. Arbitrage-free IV surfaces are then generated by sampling from the posterior distribution on the latent space, decoding to obtain SDE model parameters, and finally mapping those parameters to IV surfaces.

* 12 pages, 4 figures

View paper on