Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeApplication of Deep Neural Networks to assess corporate Credit Rating

Paper and Code

Mar 04, 2020

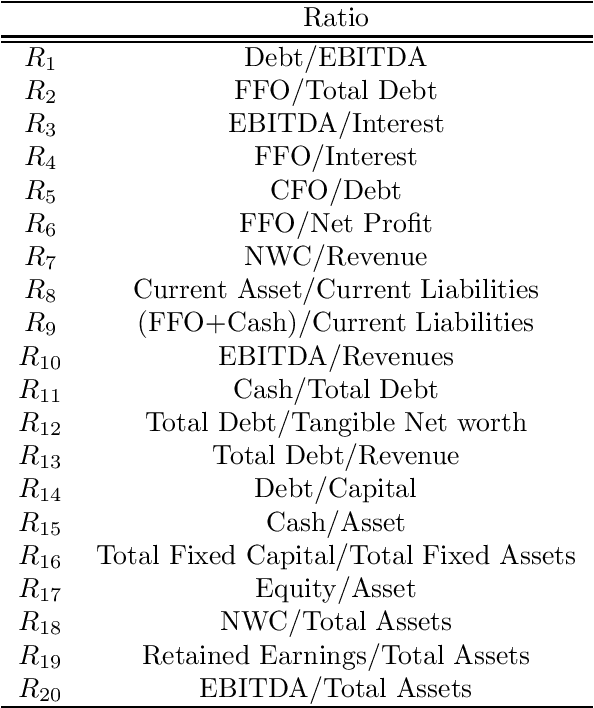

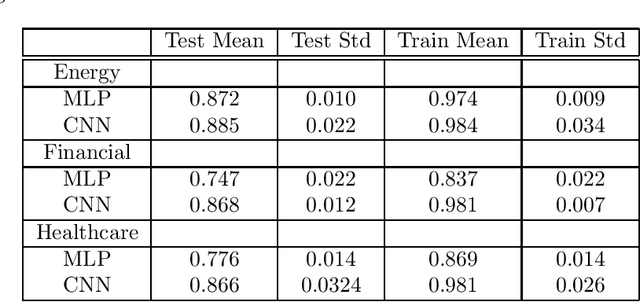

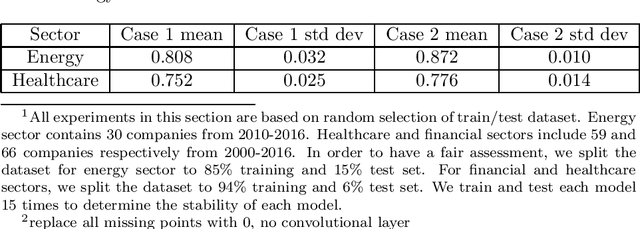

Recent literature implements machine learning techniques to assess corporate credit rating based on financial statement reports. In this work, we analyze the performance of four neural network architectures (MLP, CNN, CNN2D, LSTM) in predicting corporate credit rating as issued by Standard and Poor's. We analyze companies from the energy, financial and healthcare sectors in US. The goal of the analysis is to improve application of machine learning algorithms to credit assessment. To this end, we focus on three questions. First, we investigate if the algorithms perform better when using a selected subset of features, or if it is better to allow the algorithms to select features themselves. Second, is the temporal aspect inherent in financial data important for the results obtained by a machine learning algorithm? Third, is there a particular neural network architecture that consistently outperforms others with respect to input features, sectors and holdout set? We create several case studies to answer these questions and analyze the results using ANOVA and multiple comparison testing procedure.