Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeAdversarial Estimation of Riesz Representers

Paper and Code

Dec 30, 2020

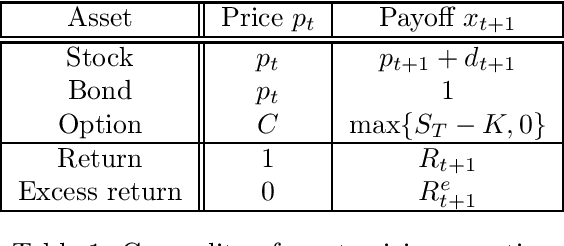

We provide an adversarial approach to estimating Riesz representers of linear functionals within arbitrary function spaces. We prove oracle inequalities based on the localized Rademacher complexity of the function space used to approximate the Riesz representer and the approximation error. These inequalities imply fast finite sample mean-squared-error rates for many function spaces of interest, such as high-dimensional sparse linear functions, neural networks and reproducing kernel Hilbert spaces. Our approach offers a new way of estimating Riesz representers with a plethora of recently introduced machine learning techniques. We show how our estimator can be used in the context of de-biasing structural/causal parameters in semi-parametric models, for automated orthogonalization of moment equations and for estimating the stochastic discount factor in the context of asset pricing.