Get our free extension to see links to code for papers anywhere online!Free add-on: code for papers everywhere!Free add-on: See code for papers anywhere!

Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeA Projection Based Conditional Dependence Measure with Applications to High-dimensional Undirected Graphical Models

Paper and Code

Feb 14, 2017

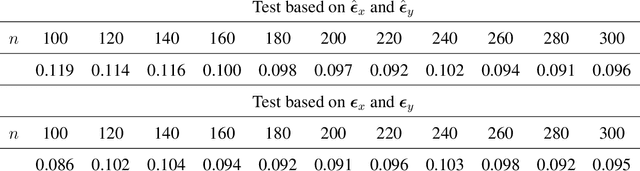

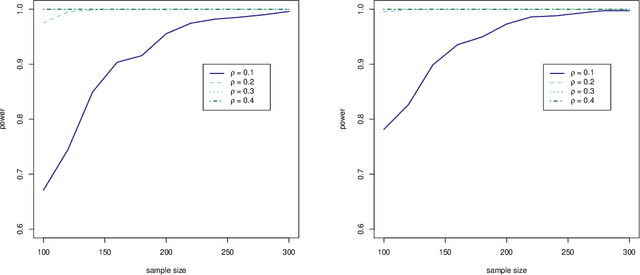

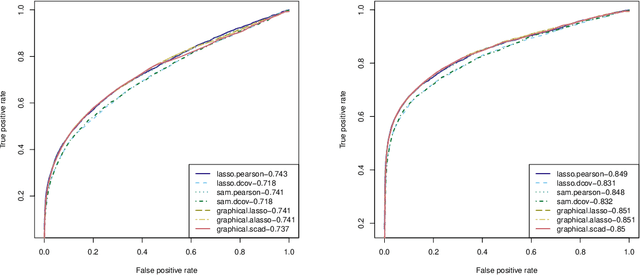

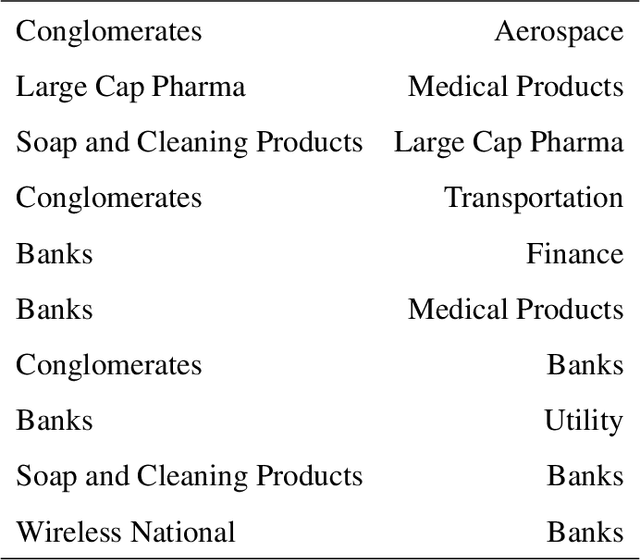

Measuring conditional dependence is an important topic in statistics with broad applications including graphical models. Under a factor model setting, a new conditional dependence measure based on projection is proposed. The corresponding conditional independence test is developed with the asymptotic null distribution unveiled where the number of factors could be high-dimensional. It is also shown that the new test has control over the asymptotic significance level and can be calculated efficiently. A generic method for building dependency graphs without Gaussian assumption using the new test is elaborated. Numerical results and real data analysis show the superiority of the new method.

* 35 pages, 7 figures

View paper on