Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeA Deep Learning Framework for Pricing Financial Instruments

Paper and Code

Sep 07, 2019

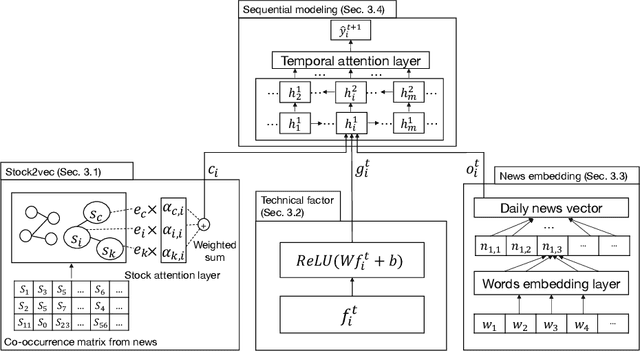

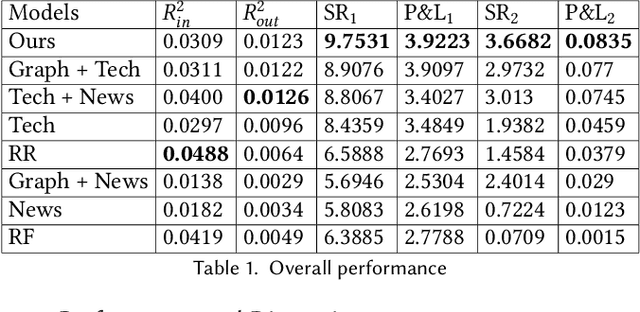

We propose an integrated deep learning architecture for the stock movement prediction. Our architecture simultaneously leverages all available alpha sources. The sources include technical signals, financial news signals, and cross-sectional signals. Our architecture possesses three main properties. First, our architecture eludes overfitting issues. Although we consume a large number of technical signals but has better generalization properties than linear models. Second, our model effectively captures the interactions between signals from different categories. Third, our architecture has low computation cost. We design a graph-based component that extracts cross-sectional interactions which circumvents usage of SVD that's needed in standard models. Experimental results on the real-world stock market show that our approach outperforms the existing baselines. Meanwhile, the results from different trading simulators demonstrate that we can effectively monetize the signals.