Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeSafe-FinRL: A Low Bias and Variance Deep Reinforcement Learning Implementation for High-Freq Stock Trading

Jun 13, 2022

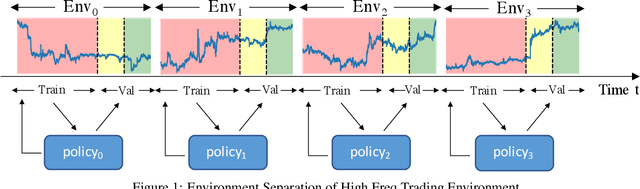

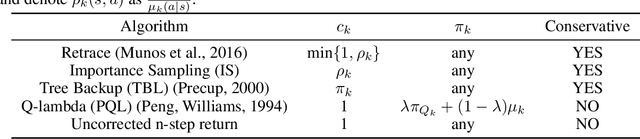

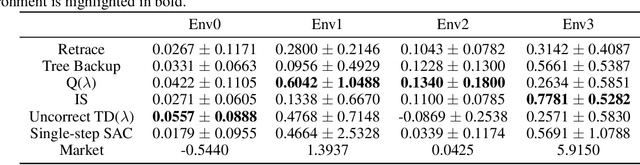

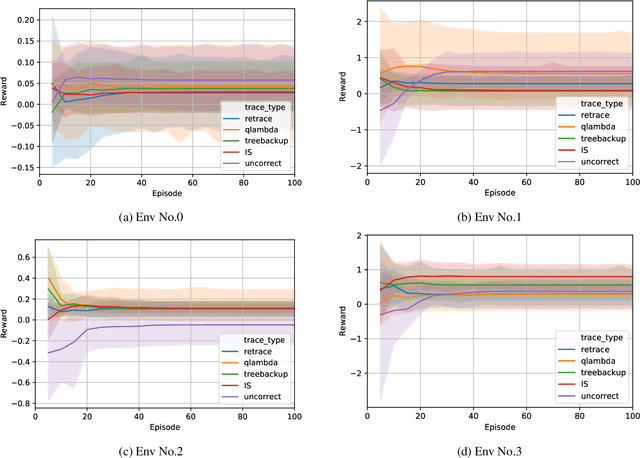

In recent years, many practitioners in quantitative finance have attempted to use Deep Reinforcement Learning (DRL) to build better quantitative trading (QT) strategies. Nevertheless, many existing studies fail to address several serious challenges, such as the non-stationary financial environment and the bias and variance trade-off when applying DRL in the real financial market. In this work, we proposed Safe-FinRL, a novel DRL-based high-freq stock trading strategy enhanced by the near-stationary financial environment and low bias and variance estimation. Our main contributions are twofold: firstly, we separate the long financial time series into the near-stationary short environment; secondly, we implement Trace-SAC in the near-stationary financial environment by incorporating the general retrace operator into the Soft Actor-Critic. Extensive experiments on the cryptocurrency market have demonstrated that Safe-FinRL has provided a stable value estimation and a steady policy improvement and reduced bias and variance significantly in the near-stationary financial environment.