Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeDesign and Optimization of Big Data and Machine Learning-Based Risk Monitoring System in Financial Markets

Jul 28, 2024

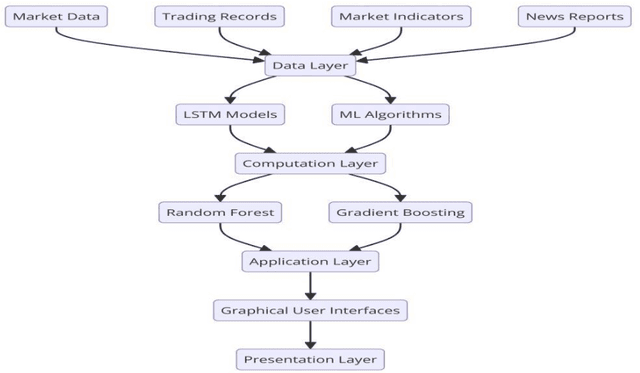

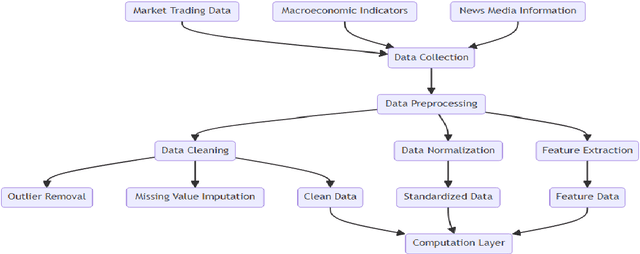

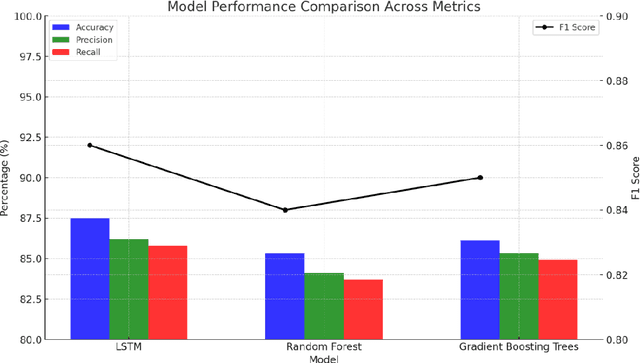

With the increasing complexity of financial markets and rapid growth in data volume, traditional risk monitoring methods no longer suffice for modern financial institutions. This paper designs and optimizes a risk monitoring system based on big data and machine learning. By constructing a four-layer architecture, it effectively integrates large-scale financial data and advanced machine learning algorithms. Key technologies employed in the system include Long Short-Term Memory (LSTM) networks, Random Forest, Gradient Boosting Trees, and real-time data processing platform Apache Flink, ensuring the real-time and accurate nature of risk monitoring. Research findings demonstrate that the system significantly enhances efficiency and accuracy in risk management, particularly excelling in identifying and warning against market crash risks.