Get our free extension to see links to code for papers anywhere online!Free add-on: code for papers everywhere!Free add-on: See code for papers anywhere!

Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgecCorrGAN: Conditional Correlation GAN for Learning Empirical Conditional Distributions in the Elliptope

Jul 22, 2021

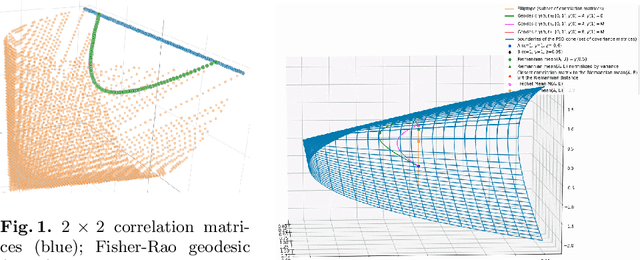

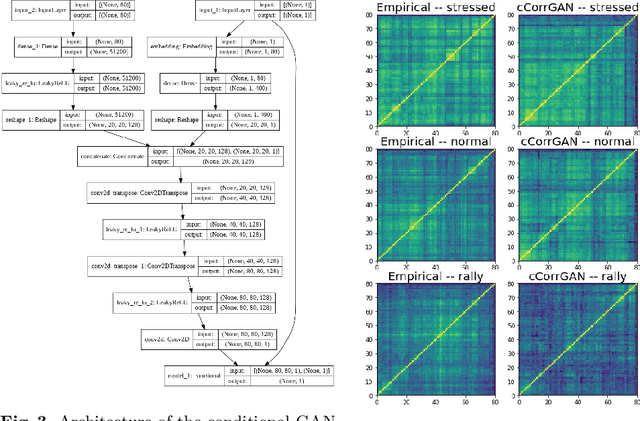

We propose a methodology to approximate conditional distributions in the elliptope of correlation matrices based on conditional generative adversarial networks. We illustrate the methodology with an application from quantitative finance: Monte Carlo simulations of correlated returns to compare risk-based portfolio construction methods. Finally, we discuss about current limitations and advocate for further exploration of the elliptope geometry to improve results.

* GSI 2021: Geometric Science of Information pp 613-620

* International Conference on Geometric Science of Information

* International Conference on Geometric Science of Information

Via