Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeSupervised Neural Networks for Illiquid Alternative Asset Cash Flow Forecasting

Aug 05, 2021

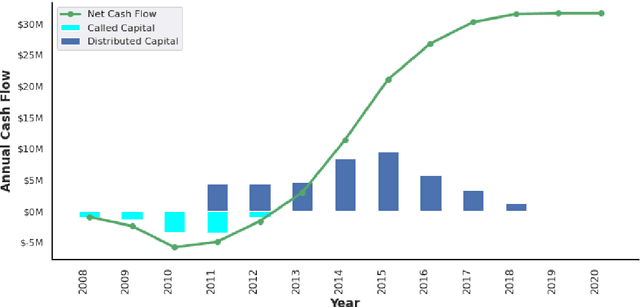

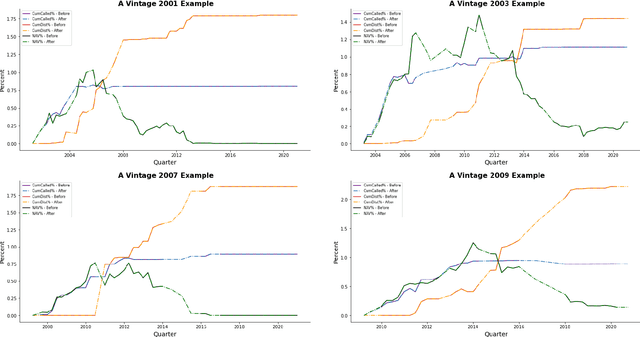

Institutional investors have been increasing the allocation of the illiquid alternative assets such as private equity funds in their portfolios, yet there exists a very limited literature on cash flow forecasting of illiquid alternative assets. The net cash flow of private equity funds typically follow a J-curve pattern, however the timing and the size of the contributions and distributions depend on the investment opportunities. In this paper, we develop a benchmark model and present two novel approaches (direct vs. indirect) to predict the cash flows of private equity funds. We introduce a sliding window approach to apply on our cash flow data because different vintage year funds contain different lengths of cash flow information. We then pass the data to an LSTM/ GRU model to predict the future cash flows either directly or indirectly (based on the benchmark model). We further integrate macroeconomic indicators into our data, which allows us to consider the impact of market environment on cash flows and to apply stress testing. Our results indicate that the direct model is easier to implement compared to the benchmark model and the indirect model, but still the predicted cash flows align better with the actual cash flows. We also show that macroeconomic variables improve the performance of the direct model whereas the impact is not obvious on the indirect model.

Two-Stage Sector Rotation Methodology Using Machine Learning and Deep Learning Techniques

Aug 05, 2021

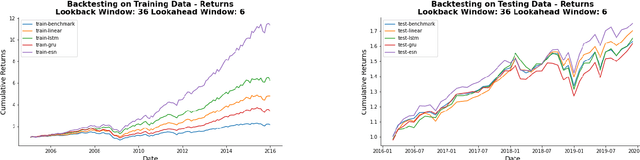

Market indicators such as CPI and GDP have been widely used over decades to identify the stage of business cycles and also investment attractiveness of sectors given market conditions. In this paper, we propose a two-stage methodology that consists of predicting ETF prices for each sector using market indicators and ranking sectors based on their predicted rate of returns. We initially start with choosing sector specific macroeconomic indicators and implement Recursive Feature Elimination algorithm to select the most important features for each sector. Using our prediction tool, we implement different Recurrent Neural Networks models to predict the future ETF prices for each sector. We then rank the sectors based on their predicted rate of returns. We select the best performing model by evaluating the annualized return, annualized Sharpe ratio, and Calmar ratio of the portfolios that includes the top four ranked sectors chosen by the model. We also test the robustness of the model performance with respect to lookback windows and look ahead windows. Our empirical results show that our methodology beats the equally weighted portfolio performance even in the long run. We also find that Echo State Networks exhibits an outstanding performance compared to other models yet it is faster to implement compared to other RNN models.

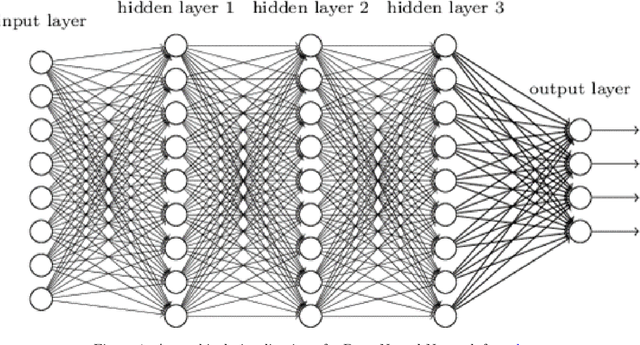

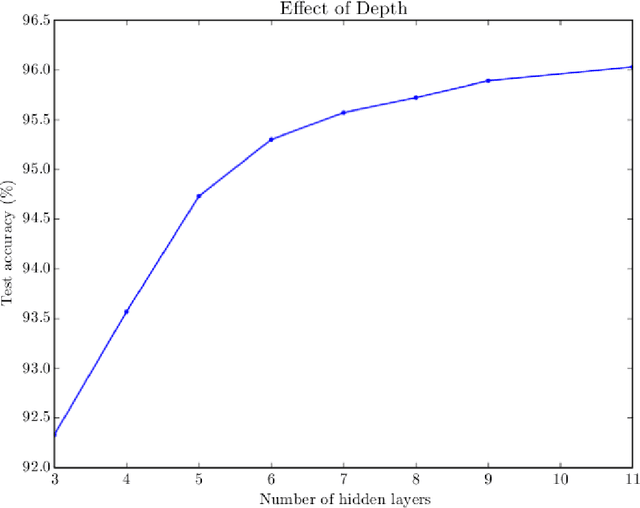

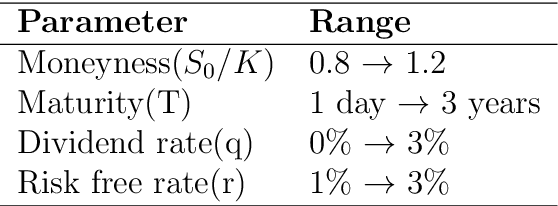

Supervised Deep Neural Networks (DNNs) for Pricing/Calibration of Vanilla/Exotic Options Under Various Different Processes

Feb 15, 2019

We apply supervised deep neural networks (DNNs) for pricing and calibration of both vanilla and exotic options under both diffusion and pure jump processes with and without stochastic volatility. We train our neural network models under different number of layers, neurons per layer, and various different activation functions in order to find which combinations work better empirically. For training, we consider various different loss functions and optimization routines. We demonstrate that deep neural networks exponentially expedite option pricing compared to commonly used option pricing methods which consequently make calibration and parameter estimation super fast.