Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeSupervised Neural Networks for Illiquid Alternative Asset Cash Flow Forecasting

Paper and Code

Aug 05, 2021

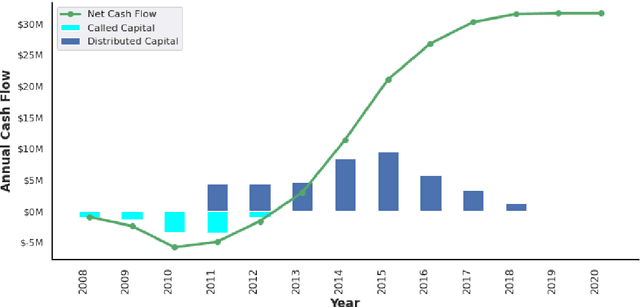

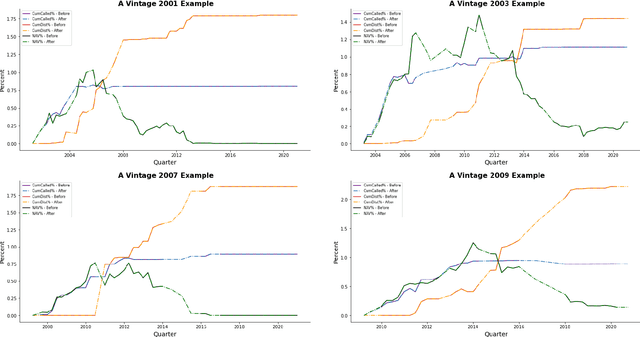

Institutional investors have been increasing the allocation of the illiquid alternative assets such as private equity funds in their portfolios, yet there exists a very limited literature on cash flow forecasting of illiquid alternative assets. The net cash flow of private equity funds typically follow a J-curve pattern, however the timing and the size of the contributions and distributions depend on the investment opportunities. In this paper, we develop a benchmark model and present two novel approaches (direct vs. indirect) to predict the cash flows of private equity funds. We introduce a sliding window approach to apply on our cash flow data because different vintage year funds contain different lengths of cash flow information. We then pass the data to an LSTM/ GRU model to predict the future cash flows either directly or indirectly (based on the benchmark model). We further integrate macroeconomic indicators into our data, which allows us to consider the impact of market environment on cash flows and to apply stress testing. Our results indicate that the direct model is easier to implement compared to the benchmark model and the indirect model, but still the predicted cash flows align better with the actual cash flows. We also show that macroeconomic variables improve the performance of the direct model whereas the impact is not obvious on the indirect model.