Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeSIMSHIFT: A Benchmark for Adapting Neural Surrogates to Distribution Shifts

Jun 13, 2025Neural surrogates for Partial Differential Equations (PDEs) often suffer significant performance degradation when evaluated on unseen problem configurations, such as novel material types or structural dimensions. Meanwhile, Domain Adaptation (DA) techniques have been widely used in vision and language processing to generalize from limited information about unseen configurations. In this work, we address this gap through two focused contributions. First, we introduce SIMSHIFT, a novel benchmark dataset and evaluation suite composed of four industrial simulation tasks: hot rolling, sheet metal forming, electric motor design and heatsink design. Second, we extend established domain adaptation methods to state of the art neural surrogates and systematically evaluate them. These approaches use parametric descriptions and ground truth simulations from multiple source configurations, together with only parametric descriptions from target configurations. The goal is to accurately predict target simulations without access to ground truth simulation data. Extensive experiments on SIMSHIFT highlight the challenges of out of distribution neural surrogate modeling, demonstrate the potential of DA in simulation, and reveal open problems in achieving robust neural surrogates under distribution shifts in industrially relevant scenarios. Our codebase is available at https://github.com/psetinek/simshift

Explainable Machine Learning-driven Strategy for Automated Trading Pattern Extraction

Apr 13, 2021

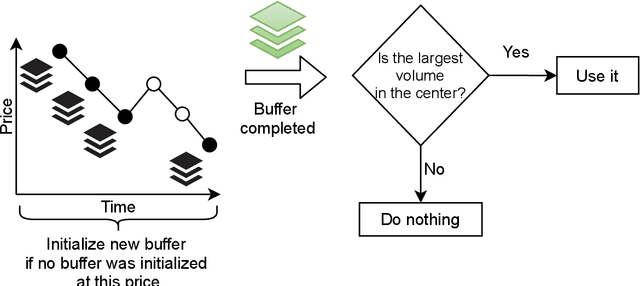

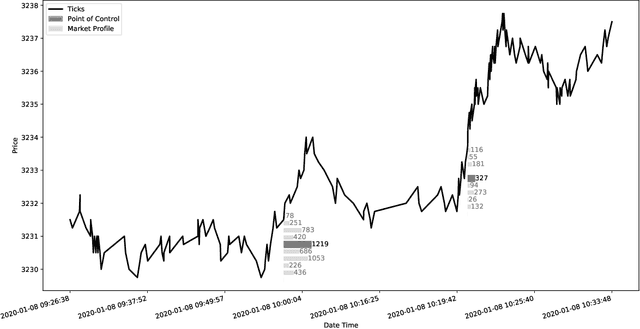

Financial markets are a source of non-stationary multidimensional time series which has been drawing attention for decades. Each financial instrument has its specific changing over time properties, making their analysis a complex task. Improvement of understanding and development of methods for financial time series analysis is essential for successful operation on financial markets. In this study we propose a volume-based data pre-processing method for making financial time series more suitable for machine learning pipelines. We use a statistical approach for assessing the performance of the method. Namely, we formally state the hypotheses, set up associated classification tasks, compute effect sizes with confidence intervals, and run statistical tests to validate the hypotheses. We additionally assess the trading performance of the proposed method on historical data and compare it to a previously published approach. Our analysis shows that the proposed volume-based method allows successful classification of the financial time series patterns, and also leads to better classification performance than a price action-based method, excelling specifically on more liquid financial instruments. Finally, we propose an approach for obtaining feature interactions directly from tree-based models on example of CatBoost estimator, as well as formally assess the relatedness of the proposed approach and SHAP feature interactions with a positive outcome.