Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeFull error analysis of the random deep splitting method for nonlinear parabolic PDEs and PIDEs with infinite activity

May 08, 2024

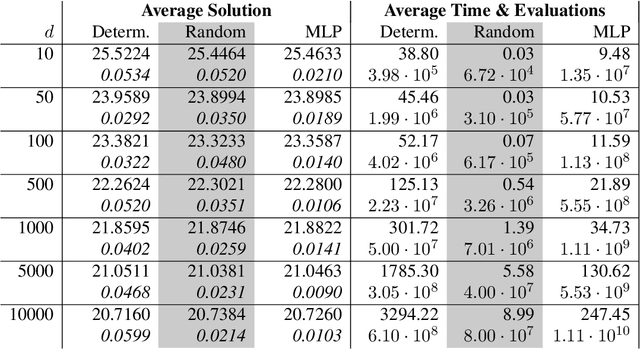

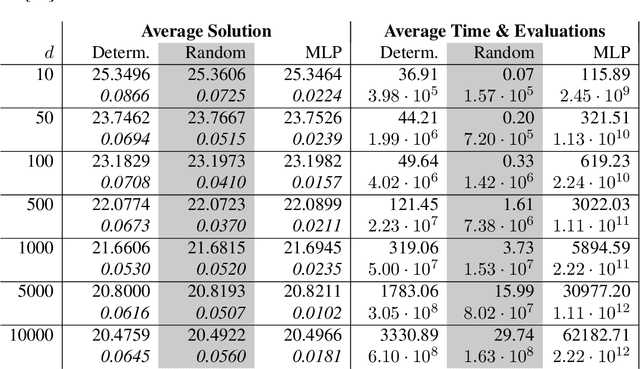

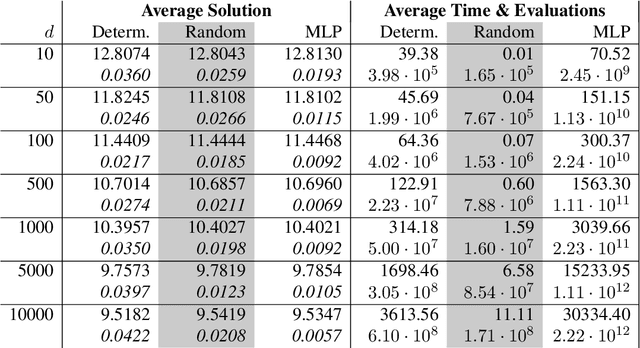

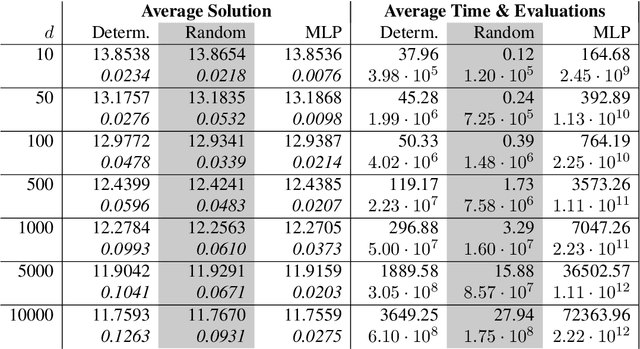

In this paper, we present a randomized extension of the deep splitting algorithm introduced in [Beck, Becker, Cheridito, Jentzen, and Neufeld (2021)] using random neural networks suitable to approximately solve both high-dimensional nonlinear parabolic PDEs and PIDEs with jumps having (possibly) infinite activity. We provide a full error analysis of our so-called random deep splitting method. In particular, we prove that our random deep splitting method converges to the (unique viscosity) solution of the nonlinear PDE or PIDE under consideration. Moreover, we empirically analyze our random deep splitting method by considering several numerical examples including both nonlinear PDEs and nonlinear PIDEs relevant in the context of pricing of financial derivatives under default risk. In particular, we empirically demonstrate in all examples that our random deep splitting method can approximately solve nonlinear PDEs and PIDEs in 10'000 dimensions within seconds.