Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgePrecise Stock Price Prediction for Optimized Portfolio Design Using an LSTM Model

Mar 02, 2022

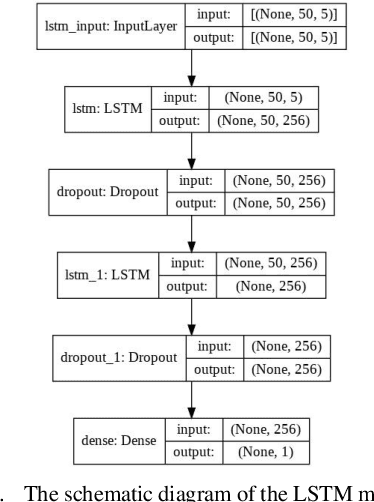

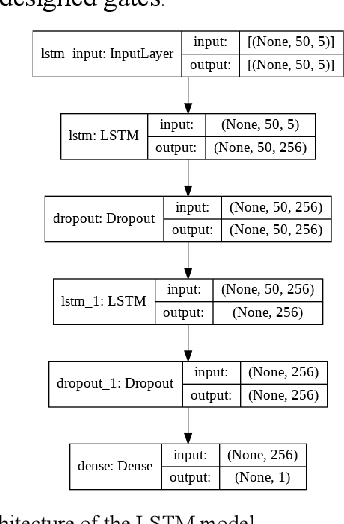

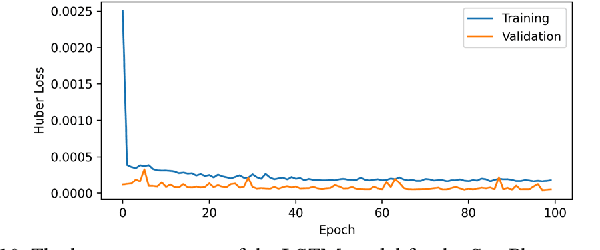

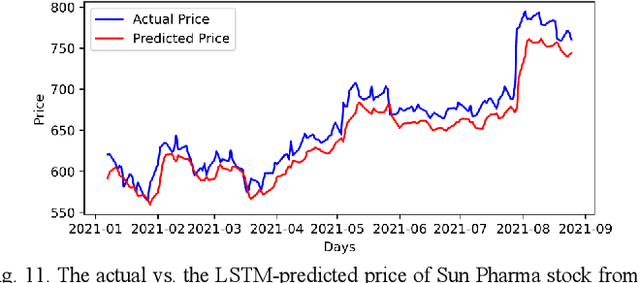

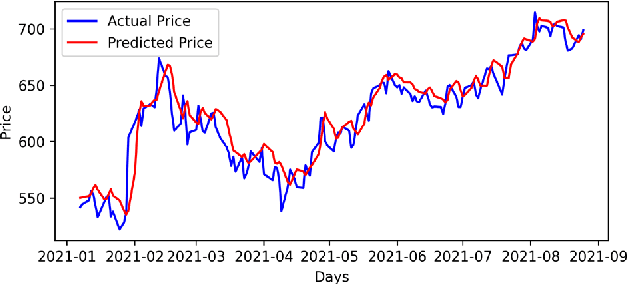

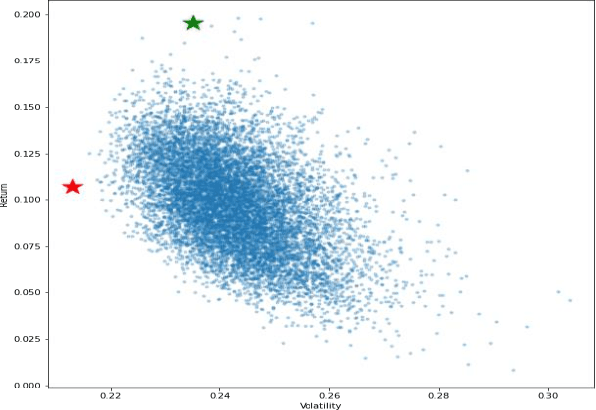

Accurate prediction of future prices of stocks is a difficult task to perform. Even more challenging is to design an optimized portfolio of stocks with the identification of proper weights of allocation to achieve the optimized values of return and risk. We present optimized portfolios based on the seven sectors of the Indian economy. The past prices of the stocks are extracted from the web from January 1, 2016, to December 31, 2020. Optimum portfolios are designed on the selected seven sectors. An LSTM regression model is also designed for predicting future stock prices. Five months after the construction of the portfolios, i.e., on June 1, 2021, the actual and predicted returns and risks of each portfolio are computed. The predicted and the actual returns indicate the very high accuracy of the LSTM model.

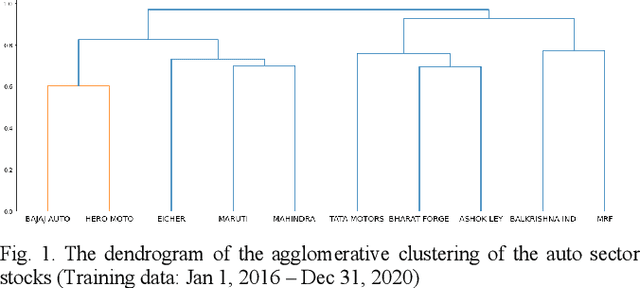

Hierarchical Risk Parity and Minimum Variance Portfolio Design on NIFTY 50 Stocks

Feb 06, 2022

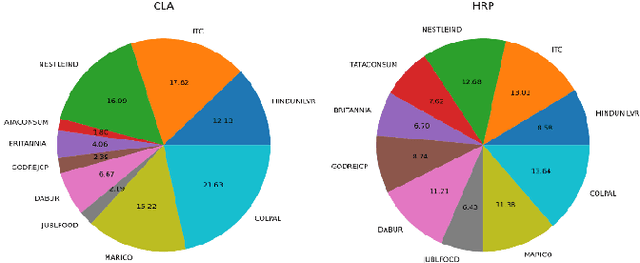

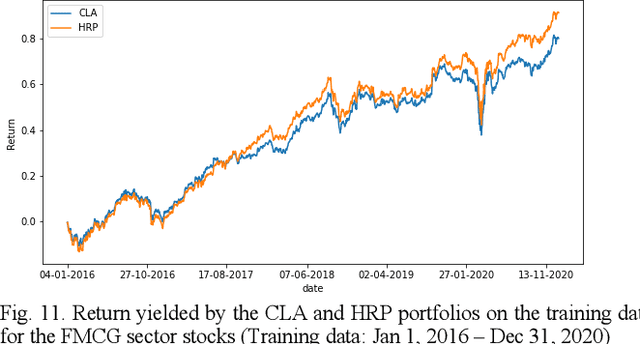

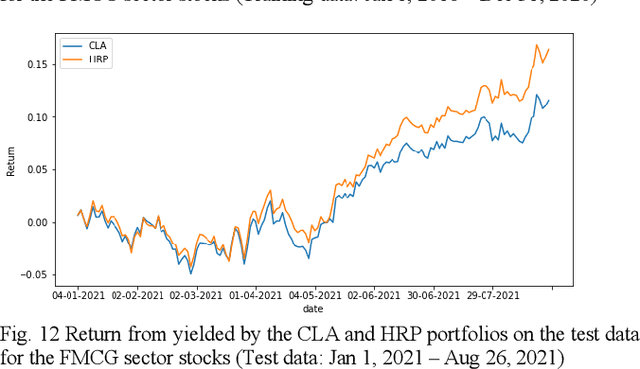

Portfolio design and optimization have been always an area of research that has attracted a lot of attention from researchers from the finance domain. Designing an optimum portfolio is a complex task since it involves accurate forecasting of future stock returns and risks and making a suitable tradeoff between them. This paper proposes a systematic approach to designing portfolios using two algorithms, the critical line algorithm, and the hierarchical risk parity algorithm on eight sectors of the Indian stock market. While the portfolios are designed using the stock price data from Jan 1, 2016, to Dec 31, 2020, they are tested on the data from Jan 1, 2021, to Aug 26, 2021. The backtesting results of the portfolios indicate while the performance of the CLA algorithm is superior on the training data, the HRP algorithm has outperformed the CLA algorithm on the test data.

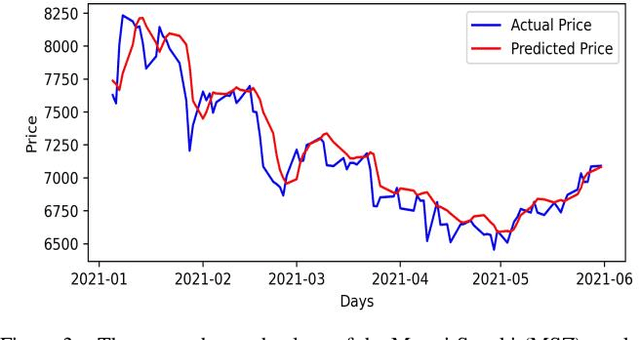

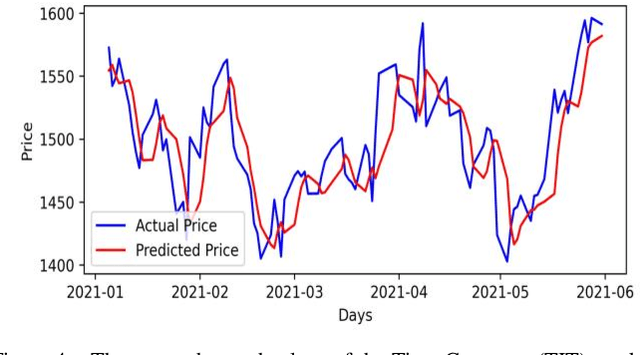

Portfolio Optimization on NIFTY Thematic Sector Stocks Using an LSTM Model

Feb 06, 2022Portfolio optimization has been a broad and intense area of interest for quantitative and statistical finance researchers and financial analysts. It is a challenging task to design a portfolio of stocks to arrive at the optimized values of the return and risk. This paper presents an algorithmic approach for designing optimum risk and eigen portfolios for five thematic sectors of the NSE of India. The prices of the stocks are extracted from the web from Jan 1, 2016, to Dec 31, 2020. Optimum risk and eigen portfolios for each sector are designed based on ten critical stocks from the sector. An LSTM model is designed for predicting future stock prices. Seven months after the portfolios were formed, on Aug 3, 2021, the actual returns of the portfolios are compared with the LSTM-predicted returns. The predicted and the actual returns indicate a very high-level accuracy of the LSTM model.

Machine Learning: Algorithms, Models, and Applications

Jan 06, 2022

Recent times are witnessing rapid development in machine learning algorithm systems, especially in reinforcement learning, natural language processing, computer and robot vision, image processing, speech, and emotional processing and understanding. In tune with the increasing importance and relevance of machine learning models, algorithms, and their applications, and with the emergence of more innovative uses cases of deep learning and artificial intelligence, the current volume presents a few innovative research works and their applications in real world, such as stock trading, medical and healthcare systems, and software automation. The chapters in the book illustrate how machine learning and deep learning algorithms and models are designed, optimized, and deployed. The volume will be useful for advanced graduate and doctoral students, researchers, faculty members of universities, practicing data scientists and data engineers, professionals, and consultants working on the broad areas of machine learning, deep learning, and artificial intelligence.

Analysis of Sectoral Profitability of the Indian Stock Market Using an LSTM Regression Model

Nov 09, 2021

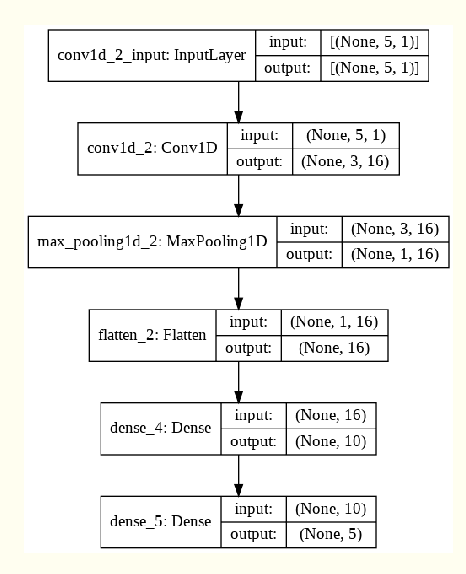

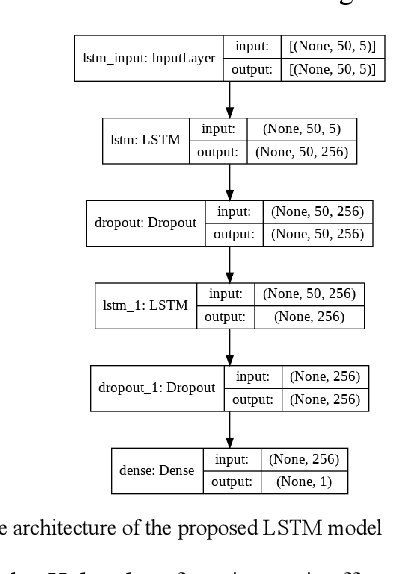

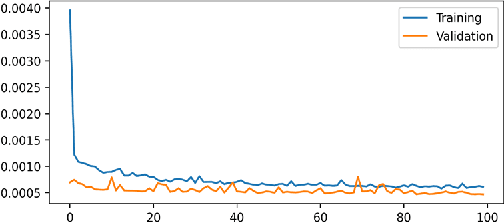

Predictive model design for accurately predicting future stock prices has always been considered an interesting and challenging research problem. The task becomes complex due to the volatile and stochastic nature of the stock prices in the real world which is affected by numerous controllable and uncontrollable variables. This paper presents an optimized predictive model built on long-and-short-term memory (LSTM) architecture for automatically extracting past stock prices from the web over a specified time interval and predicting their future prices for a specified forecast horizon, and forecasts the future stock prices. The model is deployed for making buy and sell transactions based on its predicted results for 70 important stocks from seven different sectors listed in the National Stock Exchange (NSE) of India. The profitability of each sector is derived based on the total profit yielded by the stocks in that sector over a period from Jan 1, 2010 to Aug 26, 2021. The sectors are compared based on their profitability values. The prediction accuracy of the model is also evaluated for each sector. The results indicate that the model is highly accurate in predicting future stock prices.

Stock Portfolio Optimization Using a Deep Learning LSTM Model

Nov 08, 2021

Predicting future stock prices and their movement patterns is a complex problem. Hence, building a portfolio of capital assets using the predicted prices to achieve the optimization between its return and risk is an even more difficult task. This work has carried out an analysis of the time series of the historical prices of the top five stocks from the nine different sectors of the Indian stock market from January 1, 2016, to December 31, 2020. Optimum portfolios are built for each of these sectors. For predicting future stock prices, a long-and-short-term memory (LSTM) model is also designed and fine-tuned. After five months of the portfolio construction, the actual and the predicted returns and risks of each portfolio are computed. The predicted and the actual returns of each portfolio are found to be high, indicating the high precision of the LSTM model.

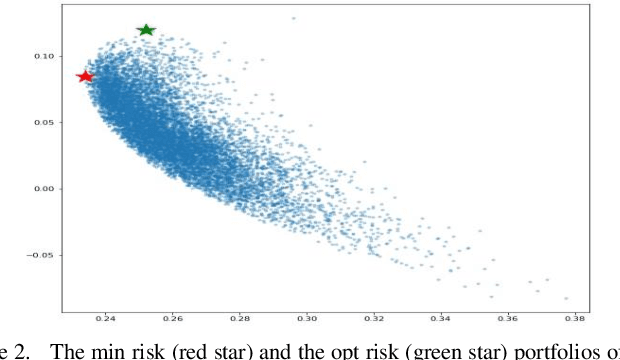

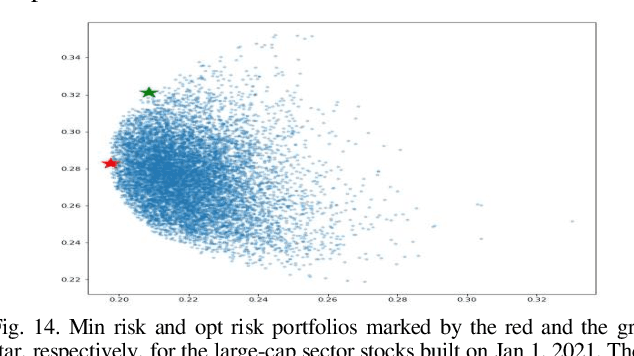

Optimum Risk Portfolio and Eigen Portfolio: A Comparative Analysis Using Selected Stocks from the Indian Stock Market

Jul 23, 2021

Designing an optimum portfolio that allocates weights to its constituent stocks in a way that achieves the best trade-off between the return and the risk is a challenging research problem. The classical mean-variance theory of portfolio proposed by Markowitz is found to perform sub-optimally on the real-world stock market data since the error in estimation for the expected returns adversely affects the performance of the portfolio. This paper presents three approaches to portfolio design, viz, the minimum risk portfolio, the optimum risk portfolio, and the Eigen portfolio, for seven important sectors of the Indian stock market. The daily historical prices of the stocks are scraped from Yahoo Finance website from January 1, 2016, to December 31, 2020. Three portfolios are built for each of the seven sectors chosen for this study, and the portfolios are analyzed on the training data based on several metrics such as annualized return and risk, weights assigned to the constituent stocks, the correlation heatmaps, and the principal components of the Eigen portfolios. Finally, the optimum risk portfolios and the Eigen portfolios for all sectors are tested on their return over a period of a six-month period. The performances of the portfolios are compared and the portfolio yielding the higher return for each sector is identified.

Design and Analysis of Robust Deep Learning Models for Stock Price Prediction

Jun 17, 2021

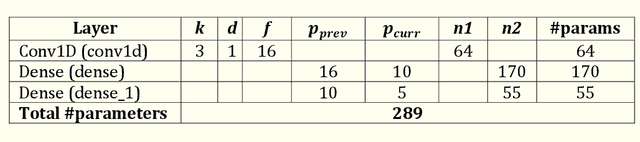

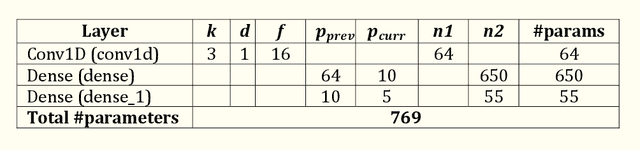

Building predictive models for robust and accurate prediction of stock prices and stock price movement is a challenging research problem to solve. The well-known efficient market hypothesis believes in the impossibility of accurate prediction of future stock prices in an efficient stock market as the stock prices are assumed to be purely stochastic. However, numerous works proposed by researchers have demonstrated that it is possible to predict future stock prices with a high level of precision using sophisticated algorithms, model architectures, and the selection of appropriate variables in the models. This chapter proposes a collection of predictive regression models built on deep learning architecture for robust and precise prediction of the future prices of a stock listed in the diversified sectors in the National Stock Exchange (NSE) of India. The Metastock tool is used to download the historical stock prices over a period of two years (2013- 2014) at 5 minutes intervals. While the records for the first year are used to train the models, the testing is carried out using the remaining records. The design approaches of all the models and their performance results are presented in detail. The models are also compared based on their execution time and accuracy of prediction.

Volatility Modeling of Stocks from Selected Sectors of the Indian Economy Using GARCH

May 28, 2021

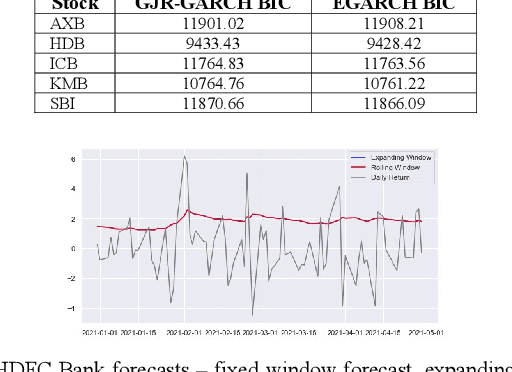

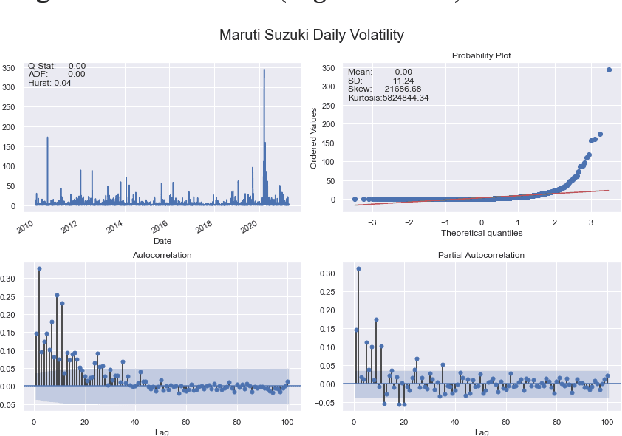

Volatility clustering is an important characteristic that has a significant effect on the behavior of stock markets. However, designing robust models for accurate prediction of future volatilities of stock prices is a very challenging research problem. We present several volatility models based on generalized autoregressive conditional heteroscedasticity (GARCH) framework for modeling the volatility of ten stocks listed in the national stock exchange (NSE) of India. The stocks are selected from the auto sector and the banking sector of the Indian economy, and they have a significant impact on the sectoral index of their respective sectors in the NSE. The historical stock price records from Jan 1, 2010, to Apr 30, 2021, are scraped from the Yahoo Finance website using the DataReader API of the Pandas module in the Python programming language. The GARCH modules are built and fine-tuned on the training data and then tested on the out-of-sample data to evaluate the performance of the models. The analysis of the results shows that asymmetric GARCH models yield more accurate forecasts on the future volatility of stocks.

Profitability Analysis in Stock Investment Using an LSTM-Based Deep Learning Model

Apr 06, 2021

Designing robust systems for precise prediction of future prices of stocks has always been considered a very challenging research problem. Even more challenging is to build a system for constructing an optimum portfolio of stocks based on the forecasted future stock prices. We present a deep learning-based regression model built on a long-and-short-term memory network (LSTM) network that automatically scraps the web and extracts historical stock prices based on a stock's ticker name for a specified pair of start and end dates, and forecasts the future stock prices. We deploy the model on 75 significant stocks chosen from 15 critical sectors of the Indian stock market. For each of the stocks, the model is evaluated for its forecast accuracy. Moreover, the predicted values of the stock prices are used as the basis for investment decisions, and the returns on the investments are computed. Extensive results are presented on the performance of the model. The analysis of the results demonstrates the efficacy and effectiveness of the system and enables us to compare the profitability of the sectors from the point of view of the investors in the stock market.