Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeAdaptive Estimation and Uniform Confidence Bands for Nonparametric IV

Jul 25, 2021

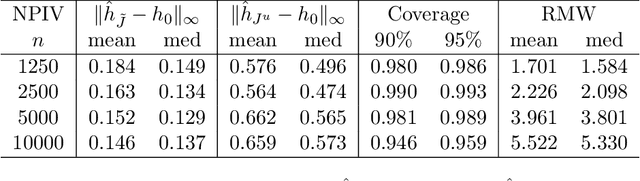

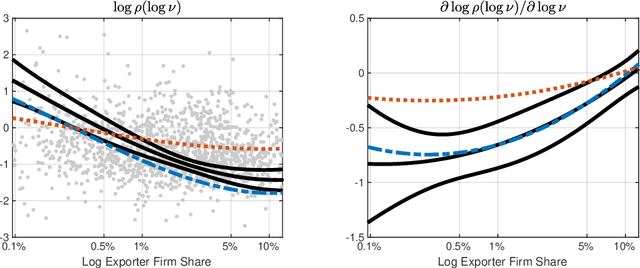

We introduce computationally simple, data-driven procedures for estimation and inference on a structural function $h_0$ and its derivatives in nonparametric models using instrumental variables. Our first procedure is a bootstrap-based, data-driven choice of sieve dimension for sieve nonparametric instrumental variables (NPIV) estimators. When implemented with this data-driven choice, sieve NPIV estimators of $h_0$ and its derivatives are adaptive: they converge at the best possible (i.e., minimax) sup-norm rate, without having to know the smoothness of $h_0$, degree of endogeneity of the regressors, or instrument strength. Our second procedure is a data-driven approach for constructing honest and adaptive uniform confidence bands (UCBs) for $h_0$ and its derivatives. Our data-driven UCBs guarantee coverage for $h_0$ and its derivatives uniformly over a generic class of data-generating processes (honesty) and contract at, or within a logarithmic factor of, the minimax sup-norm rate (adaptivity). As such, our data-driven UCBs deliver asymptotic efficiency gains relative to UCBs constructed via the usual approach of undersmoothing. In addition, both our procedures apply to nonparametric regression as a special case. We use our procedures to estimate and perform inference on a nonparametric gravity equation for the intensive margin of firm exports and find evidence against common parameterizations of the distribution of unobserved firm productivity.